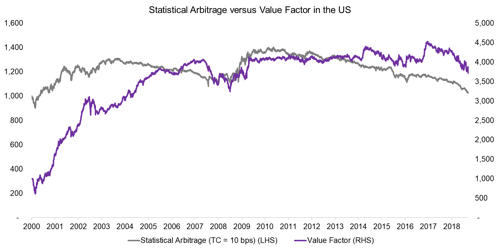

Arbitrage is the process of simultaneously buying and selling a financial instrument on different markets, In finance, statistical arbitrage is a class of short-term financial trading strategies that employ mean reversion models involving broadly diversified portfolios of securities (hundreds to thousands) held for short periods of time (generally seconds to days). Statistical arbitrage strategies are market neutral because they involve opening both a long position and short position simultaneously to take advantage of inefficient pricing in correlated securities. The end objective of such strategies is to generate alpha (higher than normal profits) for the trading firms. These strategies are supported by substantial mathematical, computational, and trading platforms. Investors typically identify arbitrage situations through mathematical modeling techniques. Those models are usually based on mean-reverting strategies and require significant computational power.

Statistical Arbitrage is an arbitrage technique that involves complex statistical models to find trading opportunities among financial instruments with different market prices. This type of trading strategy assigns stocks a desirability ranking and then constructs a portfolio to reduce risk as much as possible. These strategies look to exploit the relative price movements across thousands of financial instruments by analyzing the price patterns and the price differences between financial instruments. This arbitrage is not true arbitrage because it does not deliver a guaranteed profit — in fact, many statistical arbitrageurs have made large losses.

The various concepts used by statistical arbitrage strategies include:

- Time Series Analysis

- AutoRegression and Co-integration

- Volatility modeling

- Principal Components Analysis

- Pattern finding techniques

- Machine learning techniques

- Efficient frontier analysis etc.

Risks

Statistical arbitrage is not without risk. Over a finite period of time, a low probability market movement may impose heavy short-term losses. It depends heavily on the ability of market prices to return to a historical or predicted normal, commonly referred to as mean reversion. If such short-term losses are greater than the investor’s funding to meet interim margin calls, its positions may need to be liquidated at a loss even when its strategy’s modeled forecasts ultimately turn out to be correct. The 1998 default of Long-Term Capital Management was a widely publicized example of a fund that failed due to its inability to post collateral to cover adverse market fluctuations. The popularity of the strategy continued for more than two decades and different models were created around it to capture big profits.

Types of Statistical Arbitrage Strategies –

- Market Neutral Arbitrage – It involves taking a long position in an undervalued asset and shorting an overvalued asset simultaneously.

- Cross Asset Arbitrage – It seeks to exploit the price discrepancy of the same asset across markets.

- Cross Market Arbitrage – This model bets on the price discrepancy between a financial asset and it’s underlying.

- ETF Arbitrage – It can be termed as a form of cross-asset arbitrage that identifies discrepancies between the value of an ETF and its underlying assets.