The main objective of the study is to analyze and evaluate the treasury management procedure and performance of Berger paints Bangladesh Limited. BPBL is the market leader in the paint industry who holds 55% market Share. BPBL has eleven sales offices around the Bangladesh. The sales proceeds are collected through Citi N/A bank which is the mother bank of BPBL. The company uses SAP software for their daily financial works. This software performs the required function of speeding up the cash receipts and payments as well as provides greater accountability

which enables the management at the top to take efficient decisions in regards of the liquidity available. For efficient liquidity management Treasury department is able to make payment to its creditors as early as possible. BPBL has strong and good liquidity position and had no opportunity to run out from short-term financial solvency.

BPBL has strong and good liquidity position and had no opportunity to run out from short-term financial solvency and this ability rises gradually (Current/Quick/Cash).BPBLs most of debts consist of creditors and accrual so BPBLs borrowing cost is insignificant. As a result BPBL is in good position regarding borrowed money compared to the resources invested by the shareholders (Debt to equity ratio).BPBLs asset-liability management efficiency increased day by day. BPBL is the less leveraged company and it has lower financial risk (Total Debt Ratio).The company is also able to use its assets and equity efficiently and effectively. The company increases its sales through inventory control and was efficiently managing and selling its inventory so BPBL tied up the fewer funds.

The gross profit margin ratio is highly satisfactory and ROA shows that BPBL is more profitable. The EPS had a gradual increase trend which is a good profitability indicator of BPBL. Berger’s profit after tax has a clear indication of its financial viability. ROE under Du-Pont analysis of BPBL indicates operating efficiency, asset use efficiency and financial leverage of BPBL is reliable. Finally BPBL is showing an upward trend in every aspect of financial statements.

Objective of the Report

The study has been undertaken with the following objectives:

- To analysis the pros and cons of the conventional ideas about Treasury Management.

- To have better orientation on Product management activities in various sector and recovery of Berger paints Bangladesh Limited.

- To get an overall idea about performance of Berger paints Bangladesh Limited and its Treasury Management.

Methodology

The primary data had been collected in various ways. The different sources were: By interviewing the manager and assistant manager of Treasury department. Face to face conversations with the employees and opportunities were given by the management to work in relevant fields in BPBL. Observing various organizational procedures.

i. Secondary data were collected

- From prior research report

- From any information regarding the Painting sector

- From different books and periodicals related to the painting sector

- From Annual Report and Internet.

ii. Data collecting instruments

In-depth interviews were conducted with various managers, employees of Berger paints Bangladesh Limited. & customers of Berger paint Bangladesh Limited. A structured questionnaire was designed which was has been considered as the major tool of preparing the report.

Introduction:

Berger Paints began its painting in Bangladesh since independence. Over the decades, Berger has evolved to becoming the leading paint solution provider in this country and has diversified into every sphere of the industry – from Decorative Paints to Industrial Coatings, from Marine Coatings to Powder Coating and what not. To give a comprehensive and sustainable painting solution to the need of the industry, Berger has invested more on technology and Research & Development (R & D) than any other manufacturer in this market. It selects the raw materials from some of the best known names in the world: Mitsui, Mobil, Dupont, Hoechst and Basf are a few to name. The superior quality of Berger’s products has been possible because of support from its advanced plants and an international-standard of strict quality. Investment in technology and plant capacity is even more evident from the new factory of Berger Paints Bangladesh Limited at Savar. The state-of-the-art factory is an addition to Berger’s capacity to make it the paint-giant in Bangladesh. Not to forget about the first Double Tight Can manufacturing unit in its Chittagong factory. All, together with devotion to make it the reputed center of Basic & Applied Research in paint and Resin Technology, proof the commitment that Berger has for this industry. With its strong distribution network, Berger has reached almost every corner of Bangladesh. Nationwide Dealer Network, supported by 7 Sales Depots strategically located at Dhaka, Chittagong, Rajshahi, Khulna, Bogra, Sylhet and Comilla has an unmatched capability to answer to paint needs at almost anywhere in Bangladesh. The sheer innovation and development

drive is reflected on the various products Berger has so far launched in this market.

Critical observations and recommendations:

BPBL needs to make sure that they have a clear view of the true cash position at any point of time. Since they deal with multiple banks, it may get difficult to know the true cash standings. Treasury department should maintain safety cash balance to meet unanticipated demands of cash and keep safety foreign currency to open LC and minimize the exchange rate risk.

BPBL has strong and good liquidity position and had no opportunity to run out from short-term financial solvency and this ability rises gradually (Current/Quick/Cash).BPBLs most of debts consist of creditors and accrual so BPBLs borrowing cost is insignificant. As a result BPBL is in good position regarding borrowed money compared to the resources invested by the shareholders (Debt to equity ratio).BPBLs asset-liability management efficiency increased day by day. BPBL is the less leveraged company and it has lower financial risk (Total Debt Ratio).The company is

also able to use its assets and equity efficiently and effectively. The company increases its sales through inventory control and was efficiently managing and selling its inventory so BPBL tied up the fewer funds.

BPBL Treasury management

BPBL’s Treasury Management is responsible to deal with all the financial transactions complying all policies and practice of the company and generate required number external and internal report for all stakeholders. BPBL shows zero tolerance of treasury management, efficient receivable and payable management, minimize the corporate risk is our core area of work. The responsibility of the treasury department is the management control of future cash flows, optimal use of all available resource. An efficiency and effective Treasury Management can manage and control various risk for example market risk, credit risk and liquidity risk of BPBL. Treasury management is the creation and governance of policies and procedures that ensure the company manages financial risk successfully. Because a primary function of treasury management is to establish levels for cash or cash equivalents so that BPBL can meet its financial obligations on time, treasury management is sometimes simply referred to as cash management.

Treasury management includes management of BPBL holdings, with the ultimate goal of maximizing the firm’s liquidity and mitigating its operational, financial and reputational risk. Treasury Management includes BPBL collections, disbursements, concentration, investment and funding activities. In BPBL, it may also include trading in bonds, currencies, financial derivatives and the associated financial risk management. Berger paints Bangladesh limited has whole departments devoted to treasury management and supporting their clients’ and customers needs in this area.

BPBL Treasuries may have the following departments:

• A Fixed Income or Product Market desk that is devoted to buying and selling goods bearing securities

• A Foreign exchange or “FX” desk that buys and sells currencies

• A Capital Markets or Equities desk that deals in shares listed on the stock market.

In addition the Treasury function may also have a Proprietary Trading desk that conducts trading activities for BPBLs’ capital BPBL may or may not disclose the prices they charge for Treasury Management products, however the Phoenix Hecht Blue Book of Pricing may be a useful source of regional pricing information by product.

Integrated business planning (IBP):

Integrated business planning is a strategy for connecting the planning functions of each department in BPBL to align operations and strategy with the BPBL’s financial performance. IBP evolved from sales and operations planning (S&OP), a multi-departmental process for forecasting demand and ensuring that the necessary supply is available. It is sometimes part of a broader budgeting, planning and forecasting (BP&F) process and relies on information

technology to prepare departmental plans and combine them into a single plan of BPBL. Several categories of software are available to help automate IBP, including the transaction software of such departments as finance, sales and manufacturing as well as S&OP, corporate performance management and analytics software.

Financial supply chain management:

BPBL, Financial supply chain management (FSCM) is a set of software tools and processes designed to enhance an organization’s product flow, maximizing profitability and minimizing expenses. To accomplish this objective, FSCM takes advantage of principles that have proven effective in supply chain management for decades.

Financial management system:

A financial management system is the methodology that BPBL uses to oversee and govern its income, expenses, and assets with the objectives of maximizing profits and ensuring sustainability. An effective financial management system improves short- and long-term business performance by streamlining invoicing and bill collection, eliminating accounting errors, minimizing record-keeping redundancy, ensuring compliance with tax and accounting regulations, helping personnel to quantify budget planning, and offering flexibility and

expandability to accommodate change and growth.

Other significant features of a good financial management system of BPBL include:

- Depreciating assets according to accepted schedules.

- Keeping all payments and receivables transparent. Amortizing prepaid expenses

- Keeping track of liabilities.

- Coordinating income statements, expense statements, and balance sheets.

- Balancing multiple bank accounts.

- Ensuring data integrity and security.

- Keeping all records up to date.

- Maintaining a complete and accurate audit trail.

- Minimizing overall paperwork.

ERP financial management software should include features that support creation of ad hoc reporting as well as month-end closing, quarter closings and year-end reporting.

Financial data management:

For Berger Paints Bangladesh Limited, the term “financial data” refers to information on performance in terms of income, expenses, and profits, usually over the course of a full fiscal year. For an individual or small business, the term “financial data” refers to bank account information, debts, assets, and credit ratings.

A well-designed FDM program can help BPBL to develop and maintain its own set of accounting procedures, streamline its internal workflow processes to minimize overhead and expense while maximizing efficiency and profit, consolidate data from among various departments, and generate custom financial reports and documents for a diverse set of suppliers and clients.

Treasury management software:

The corporate treasury space is changing fast, analysts say, and more companies are beginning a push to standardize and optimize treasury functions across the enterprise. The right treasury management software, if implemented well, enables the treasury department to do its job better and more efficiently. But buyers shouldn’t go into the process blind. Experts caution that organizations aiming to make the best use of cash while managing risks more efficiently by deploying treasury management software should carefully choose a partner vendor and take a look behind the curtain to know what they’re truly buying. Armed with the right questions and a clear idea of the potential advantages, buyers can confidently enter the market as informed consumers.

The advantages of automating treasury management:

For Berger Paints Bangladesh Limited, treasury functions are still mostly manual and fragmented among bits and pieces of legacy software scattered across the BPBL. A paradigm shift is occurring in the way BPBL look at treasury management, There’s now demand for an all-in-one, comprehensive system that allows treasury to automate, manage and report on all elements of cash, liquidity and risk management.

According to BPBL, treasury management software automates treasury processes, which helps companies optimize the use of cash and other liquid assets generated by business operations. But managing working capital isn’t the only benefit of treasury management software. Treasury is also really important in understanding what the current cash position is and managing liquidity in the short term.

BPBL underscored the importance of this benefit. Risk management is by and far the most significant driver that BPBL seen recently in the need for treasury technology. The financial crisis made it clear that no one knows what’s around the corner. Since the crisis, the spotlight was put on the treasury department to provide answers to questions around counterparty risk and liquidity risk, as well as the effective management of working capital.

Dig deep when selecting treasury management software:

There are three key elements to look for when evaluating a treasury management software system of BPBL:

Expertise. Partner with a vendor that can offer insight around the changing dynamics of the treasury space and provide sound knowledge about how the application can adapt with BPBL.

Comprehensive functionality. Clearly identify the organization’s functional requirements, and find a product built on proven industry best practices that can deal with those needs today and down the road. Platform. Choose a platform that can nimbly adjust to the environment of BPBL.

Evaluating ERP treasury modules against specialty systems:

Some would argue that they don’t need specialized software for treasury functions. BPBL have an ERP system already. BPBL have SAP, or Oracle or JD Edwards. Why do BPBL need a special piece of technology to help BPBL manage their business?”

While these ERP systems do have treasury modules, they are more interested in the transactions than they are in balances. BPBL don’t think systems are really designed to be the special-purpose tools treasuries need.

But one thing is sure — Morris expects a much more efficient future once treasury management software is in place. While compiling the cash position and forecast currently takes four hours a day, BPBL estimates this time will be cut back to a half-hour after implementing a new system. In addition, Morris is also looking forward to having more real. Information is power and it allows you to make the best decisions. BPBL won’t have to wait until the end of the day to understand what our cash position is … to understand what BPBL do for the rest of the week, month or year.

Plan ahead to side step treasury management system implementation:

BPBL ‘s relatively easy for treasury departments to manage a few bank accounts, but once a company has multiple banking relationships in multiple currencies with multiple risk factors spread around the globe, the job becomes quite a bit more complicated. That’s why, more and more, organizations are implementing treasury management systems to help rein in the variety of complex treasury functions. But technology alone is never a silver bullet, warn analysts. What’s more, good implementation can be as important as the technology itself — and is not without

challenges.

However, the good news is that with proper planning, well-led organizations can surpass the challenges that stand in the way of a successful implementation of BPBL.

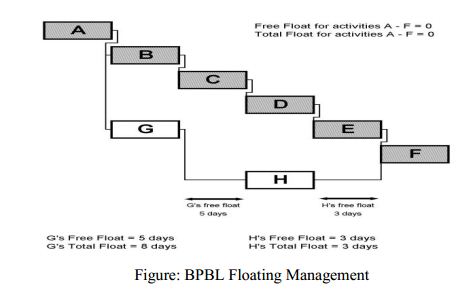

Floating Management:

BPBL Consider the process of replacing a broken pane of glass in the window of any home. There are various component activities involved in the project as a whole; obtaining the glass and putty, installing the new glass, choosing the paint, obtaining a tin once it has set, wiping the new glass free of finger smears etc. Some of these activities can run concurrently obtaining the color, obtaining the putty, choosing the paint etc., while others are consecutive the paint cannot be bought until it has been chosen, the new putty cannot be painted until the window is installed and the new putty has set. Delaying the acquisition of the glass is likely to delay the entire project – this activity will be on the critical path and have no float, of any sort, attached to it and hence it is a ‘critical activity’. A relatively short delay in the purchase of the paint may not automatically hold up the entire project as there is still some waiting time for the new putty to dry before it can be painted anyway – there will be some ‘free float’ attached to the activity of purchasing the paint and hence it is not a critical activity. However a delay in choosing the paint in turn inevitably delays buying the paint which, although it may not subsequently mean any delay to the entire project, does mean that choosing the paint has no ‘free float’ attached to it – despite having no free float of its own the choosing of the paint is involved with a path through the network which does have ‘total float’.

Collection of sales proceeds or fund:

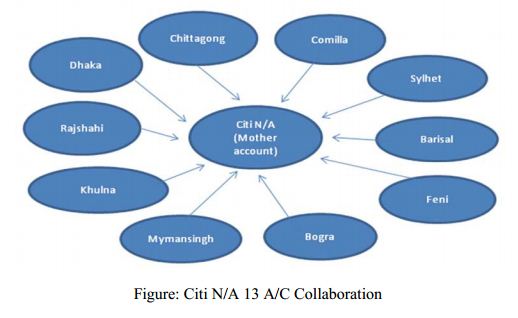

BPLB has eleven sales offices across the Bangladesh. The sales offices strategically located following districts has been enable them to strategically cater to all parts of the country.

- Dhaka sales office at Tejgoan Industrial Area

- Chittagong sales office at Chatteswari Road

- Bogra sales office at Katnar para

- Rajshahi sales office at Talaimari

- Maymansingh sales office at Maskanda

- Sylhet sales office at Antarango

- Commila sales office at AshrafpurPage

- Khulna sales office at Shabuj Baag

- Barisal sales office at south Shagordi

- Feni sales office

- Rangpur sales office

Every sales depot maintains an account in citi N/A and the sales proceeds are deposited in this account. Where Citi N/A has no branch, that location Citi N/A has collaboration with partner bank which call iti speed. In every day evening, the daily sales proceeds are transferred to Citi N/A 13 (which is known as mother account) from depot account. It is called sweep transaction.

So, the first task of account officer everyday is to check the Citi N/A account to identify total collection amount from previous day’s sales in different depots.

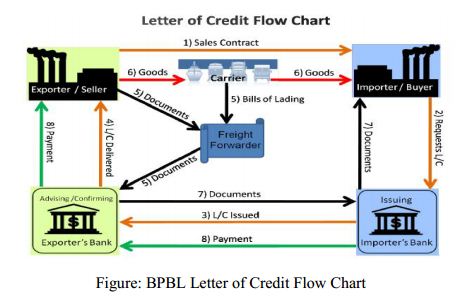

Letter of Credit (L/C) opening:

BPBL is a paint manufacturing company. It has no backward integration firm for producing needed raw materials for manufacturing paints. BPBL purchase most of the raw materials from foreign country; those countries include India, China, Singapore, German, Spain, Vietnam and so on. Letter of credit (L/C) is only method for purchasing raw materials from abroad; there is no better alternative in the business world until now. Letter of credit (L/C) is a written commitment to pay by a buyers’ or importer’s bank (called the issuing bank). BPBL mainly uses import L/C

because BPBL export an insignificant of product to abroad. BPBL opens import L/C when factory inform to supply chain department that they need a specific raw materials for producing specific paints. Factory concerned officer send specimens of raw material and supply chain department analyzes and evaluate it and contacts with foreign

suppliers. Then supply chain department contact with the issuing bank and asks to open a L/C for a specific raw materials and send pro-forma invoice to the issuing bank and the issuing bank contact with advising bank. Mainly Berger deals with following banks for L/C operation:

- Citibank N/A Limited

- Standard Chartered Bank Limited and

- Commercial Bank of Ceylon Limited

Then the treasury officers takes the initiative to settle the L/C transaction and contracts and negotiate the deal at minimum exchange rate possible on that day with either of bank mention above. The bank that provides BPBL, with favorable currency rate below the market rate usually gets the deal. This act is also known as fund purchase.

Step in the L/C opening process:

L/C Issuing Process:

The generalized process of L/C issuing in Citi N/A is explained below. For BPBL customer approached for the first time, the process will be started with opening an account with the Citi N/A.

Step 1: Application in company’s letterhead pad

First of all, BPBL have to submit an application written or printed in the company’s letterhead pad. In the application BPBL have to mention the name of the products to be imported, margin and so on. The BPBL have to apply for the required forms of the Citi N/A.

Step 2: Discussion between Bank and the party

After receiving the application form, the Citi N/A pays attention to the issues mentioned below; The quoted rates are specially analyzed as there also some restrictions by the government. The products that are going to be imported are considered. Because there are restrictions by the government on some products

Step 3: Collecting forms and depositing those with necessary documents:

In this step, the BPBL collects the L/C application form, LCA Form and IMP Form from Citi N/A. These forms are to be filled up by the client. The forms and all other necessary documents are then deposited at the desk of the dealing officer.

Step 4: Checking Documents

All the documents are checked out by the dealing officer. BPBL checks specially the quoted rates, the terms and conditions of the indent or pro forma invoice and the validity of the documents. Generally the person from whom the forms are collected is engaged in checking out the documents.

Step 5: Putting L/C No.

After checking the documents and L/C No. is given. Generally the officer who checks the documents puts the L/C No.

Step 6: Preparing offering sheet

The offering sheet is prepared by the dealing officer. Usually the officer who checks the documents prepares the offering sheet.

Step 7: Singing offering sheet

The offering sheet is then signed by the officer having the authority to open the L/C of the specified amount. If it is within the maximum limit of the amount (for which the L/C is applied) of the SAVP or branch manager, he can sign it. But if it is beyond BPBL limit proposal must be sent to the head office, either for case-to-case sanction or for credit limit. Generally, in Citi N/A, SAVP or branch managers forward the documents to the head office to approve L/C authorize.

Step 8: Typing the L/C

After the approval of opening L/C is given, the L/C is typed in a structured format.

Step 9: Checking the L/C

A final check is done to find out any discrepancies after the typing is completed. This is done by the dealing officer who is generally in charge of the whole process.

Step 10: Crediting the account of the customer

On the basis of credit arrangement with the bank of r import financing, the customer’s account is affected with certain credit.

Step 11: Dispatching L/C

At the final stage, the L/C is dispatched through postage mail or telex or SWIFT or so forth. Although this is the generalized process for issuing L/C, for the speed of the process sometimes the typing and checking of documents are done before the offering sheet is signed. Then after signing the L/C it is dispatched.

Settlement of L/C:

Settlement means fulfilling the commitment of issuing bank is regard to effect payment subject to satisfying the credit terms fully.

1. Settlement of Payment

2. Settlement of Acceptance

3. Settlement of Negotiation

1. Settlement of Payment

Here the BPBL presents the doc to the paying Citi N/A. In compliance presentation paying Citi N/A makes payment to the beneficiary and in case this Citi N/A is other than the issuing Citi N/A, then sends the doc to the issuing Citi N/A. If the issuing bank is satisfied with the requirements, payment is obtained by the paying bank from the issuing Citi N/A.

2. Settlement of Acceptance

Under this arrangement, seller submits the documents evidencing the shipment to the accepting Citi N/A accompanied by the draft drawn on Citi N/A at the specified tenor. After being satisfied with the documents, the Citi N/A accepts the docs and draft if it is Citi N/A other than the issuing Citi N/A, then sends the docs to the issuing Citi N/A stating that it has accepted the draft and at maturity the reimbursement will be obtained in the pre-agreed manner.

3. Settlement of Negotiation

This settlement procedure starts with the submission of docs by the seller to the negotiating Citi N/A accompanied by the draft drawn on the drawer at sight or at a tenor, as specified in the credit. After scrutinizing that the docs meet the credit requirements, the Citi N/A may negotiate the draft. This Citi N/A, if other than the issuing Citi N/A, then sends the docs and the draft to the issuing Citi N/A. As usual, reimbursement will be obtained in the pre-agreed manner.

The Cash Flow Budget:

This is a prediction of future cash receipts and expenditures for a particular time period of BPBL. It usually covers a period in the short term future. The cash flow budget helps BPBL determine when income will be sufficient to cover expenses and when BPBL will need to seek outside financing.

In its simplest form, cash flow is the movement of money in and out of BPBL. It could be described as the process in which BPBL uses cash to generate goods or services for the sale to its customers, collects the cash from the sales and then completes this cycle all over again.

- Keeping Inflows Flowing to BPBL

- Delaying Outflows as Long as Possible

- Profit and Loss (Income) Statements

- Balance Sheets

Cash Flow Cycle:

The direct method for creating a cash flow statement reports major classes of gross cash receipts and payments. Under BPBL, dividends received may be reported under operating activities or under investing activities. If taxes paid are directly linked to operating activities, they are reported under operating activities; if the taxes are directly linked to investing activities or financing activities, they are reported under investing or financing activities.

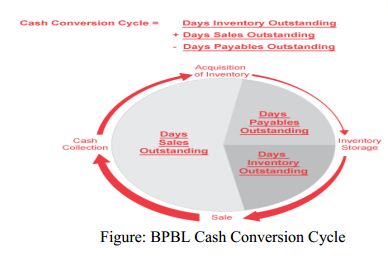

Understanding The Cash Conversion Cycle (CCC):

Usually a BPBL acquires inventory on credit, which results in accounts payable. BPBL can also sell products on credit, which results in accounts receivable. Cash, therefore, is not involved until BPBL pays the accounts payable and collects accounts receivable. So the cash conversion cycle measures the time between outlay of cash and cash recovery. The cash conversion cycle (CCC) is one of several measures of management effectiveness. It measures how fast BPBL can convert cash on hand into even more cash on hand. The CCC does this by following the cash as it is first converted into inventory and accounts payable (AP), through sales and accounts receivable (AR), and then back into cash. Generally, the lower this number is the better for BPBL. It will be explained how CCC works and show you how to use it to evaluate potential investments.

The Calculation:

To calculate CCC, BPBL need several items from the financial statements: Revenue and cost of goods sold (COGS) from the income statement; Inventory at the beginning and end of the time period; AR at the beginning and end of the time period; AP at the beginning and end of the time period; and The number of days in the period (year = 365 days, quarter = 90).

Inventory, AR and AP are found on two different balance sheets. If the period is a quarter, then use the balance sheets for the quarter in question and the ones from the preceding period. For a yearly period, use the balance sheets for the quarter in question and the one from the same quarter a year earlier. This is because while the income statement covers everything that happened over a certain time period, balance sheets are only snapshots of what the company was like at a particular moment in time. For things like AP, you want an average over the time period you are investigating, which means that AP from both the time period’s end and beginning are needed for the calculation.

Now that BPBL have some background on what goes into calculating CCC, let’s look at the formula:

CCC = DIO + DSO – DPO

Let’s look at each component and how it relates to BPBL activities discussed above. Days Inventory Outstanding (DIO): This addresses the question of how many days it takes to sell the entire inventory. The smaller this number is the better.

Cash flow forecasting of BPBL:

Cash flow forecasting is important because of BPBL runs out of cash and is not able to obtain new finance, it will become insolvent. Cash flow is the life-blood of all businesses—particularly start-ups and small enterprises. As a result, it is essential that management forecast (predict) what is going to happen to cash flow to make sure BPBL has enough to survive. How often management should forecast cash flow is dependent on the financial security of BPBL. If BPBL struggling, or is keeping a watchful eye on its finances, BPBL owner should be forecasting and revising his or her cash flow on a daily basis. However, if the finances of BPBL are more stable and ‘safe’, then forecasting and revising cash flow weekly or monthly is enough. Here are the key reasons why a cash flow forecast is so important:

Identify potential shortfalls in cash balances in advance—think of the cash flow forecast as an “early warning system”. This is, by far, the most important reason for a cash flow forecast.

Make sure that BPBL can afford to pay suppliers and employees. Suppliers who don’t get paid will soon stop supplying BPBL; it is even worse if employees are not paid on time. Spot problems with customer payments—preparing the forecast encourage BPBL to look at how quickly customers are paying their debts. Note—this is not really a problem for BPBL that take most of their sales in cash/credit cards at the point of sale. As an important discipline of financial planning—the cash flow forecast is an important management process, similar to preparing BPBL budgets. External stakeholders such as banks may require a regular forecast. Certainly, if BPBL has a bank loan, the bank will want to look at the cash flow forecast at regular intervals.

The adjusted net income method starts with operating income (EBIT or EBITDA) and adds or subtracts changes in balance sheet accounts such as receivables, payables and inventories to project cash flow.

The pro-forma balance sheet (PBS) method looks straight at the projected book cash account; if all the other balance sheet accounts have been correctly forecast, cash will be correct too.

Bank Reconciliation:

Bank reconciliation is a process that explains the difference between the bank balance shown in BPBL bank statement, as supplied by the bank, and the corresponding amount shown in the organization’s own accounting records at a particular point in time. It may be easy to reconcile the difference by looking at very recent transactions in either the bank statement or BPBL’s own accounting records and seeing if some combination of them tallies with the difference to be explained. Otherwise it may be necessary to go through and match every single transaction in both sets of records since the last reconciliation, and see what transactions remain unmatched. The necessary adjustments should then be made in the cash book, or any timing differences recorded to assist with future reconciliations. BPBL’s reconciliations are generally performed by specialized accounting software though the

understanding of what occurs is important for a successful reconciliation. Also, Citi N/A reconciliation statement is a statement prepared on a particular day to reconcile Citi N/A balance as per Cash book or Bank statement showing entries causing difference between the two balances.

Daily Treasury Report:

BPBL maintains depository Citi N/A accounts throughout the country. Distributor’s agencies and sub-agencies deposit payments to the branch office into these accounts. Basically daily treasury report measure by Treasury Yield Curve Methodology: The Treasury yield curve is estimated daily using a cubic splint model. Inputs to the model are primarily bid-side yields for on-the-run Treasury securities.

Negative Yields and Nominal Constant Maturity Treasury Series Rates (CMTs). Current financial market conditions, in conjunction with extraordinary low levels of interest rates, have resulted in negative yields for some Treasury securities trading in the secondary market. Negative yields for Treasury securities most often reflect highly technical factors in Treasury markets related to the cash and repurchase agreement markets, and are at times unrelated to the

time value of money. As such, Treasury will restrict the use of negative input yields for securities used in deriving interest rates for the Treasury nominal Constant Maturity Treasury series (CMTs). Any CMT input points with negative yields will be reset to zero percent prior to use as inputs in the CMT derivation. This decision is consistent with Treasury not accepting negative yields in Treasury nominal security auctions.

In addition, given that CMTs are used in many statutorily and regulatory determined loan and credit programs as well as for setting interest rates on non-marketable government securities, establishing a floor of zero more accurately reflects borrowing costs related to various programs.

Bank Account Opening and Closing:

Bank account opening and closing is an occasional task of BPBLs treasury department. In the time of globalization a business cannot perform all activities alone or without financial partners. So that’s, BPBLs treasury department has to open bank account to perform collection and disbursement activities smoothly. Bank account opening process is given below:

1. If a bank account is needed, the decision is taken by top management for selecting suitable bank for BPBL.

2. Collection of company account from selected bank.

3. Filling up the bank account form.

4. Singing the documents by signatory persons and sending the documents to the concerned bank. BPBL appoints a person for physical communications with bank.

When BPBL no longer needs to maintain a bank account, the concerned officer takes the steps to close this account. Bank account is a simple task only by telephonic request but it needs approval from higher authority and an application must be send to the bank.

Annual Report Preparation:

BPBL has to publish Annual report in every year; it is one of the important tasks of financial department. It is mandatory to prepare and publish financial statement according to Company Act 1991 and Securities and Exchange Commission Act 1993.BPBLs financial statements have four parts:

A. Statement of Financial Position

B. Statement of Comprehensive income

C. Statement of cash Flows and

D. Statement of Changes in Equity

Every year BPBL arrange a annual general meeting approved by the managing directors and the other directors to present the annual report. In 2013, BPBLs financial statement was audited by

A. Qasem & Co. Financial statement preparation process has following stages:

1. Information collection from concerned department

2. Information collection from trial balance

3. Setting the accounting standards and principles according to SEC act and company act.

4. Reviewing and checking by the concerned officers.

5. Audited by the appointed audited firm.

6. Approval by the board of directors and signatory persons.

7. Finally publishing it to the shareholders and external and internal stakeholders.

Swap Management:

A swap is an agreement between two parties to exchange sequences of cash flows for a set period of time. The five generic types of swaps, in order of their quantitative importance are: interest rate swaps, currency swaps, credit swaps, commodity swaps and equity swaps. There are also many other types of swaps. BPBL usually two kinds of swap: Currency swap: simultaneous buying and selling of a currency to convert debt principal from the lenders currency to the debtor’s currency. A currency swap involves exchanging principal and fixed rate interest payments on a loan in one currency for principal and fixed rate interest payments on an equal loan in another currency.

Interest rate swap: Exchange of periodic interest payments between two parties (called counter parties) as means of exchanging future flows.

Foreign Exchange Rate Forecasting and Settlement:

Foreign exchange rate forecasting is one of the major tasks of treasury department. It is done for preparing foreign exchange gain and loss from L/C operations. Estimating and analyzing the exchange rate is very important for Berger paints to determine the actual gain and loss from L/C operation. Mainly the gain and loss from L/C operation is derived from the difference between the spot rate and negotiated rate with corresponding banks.

For instance, assume today’s spot rate of USD is taka 80.00 and BPBL has to negotiate for an L/C worth $40000.Suppose HSBC bank offers BPBL an exchange rate of TK 80.00 for $1, at that situation BPBL offers 79.80 for $1 then HSBC reduces price of dollar to 79.90 for $1.BPBL agrees with this rate offered by HSBC. At this rate BPBL is making a profit of tk 4000.Hence, the treasury manager strikes a deal with HSBC. In this way, BPBL makes a gain of large amount of money.

Observation:

The chart shows that, the exchange gain from foreign exchange operations is highly fluctuated from year to year. In 2012 and 2009 it had a negative growth rate 89.61% and 71.69% respectively but in 2011 it was tremendously increased by 1129.62%. It might be greatly fluctuated because of the money market situation or inefficiency of bargaining process of treasury department.

Payments of Dividend:

As BPBL is a public limited company so it has to pay dividend to stockholders. The dividend is declared by the board of directors in Annual General Meeting but it is paid by the treasury department. BPBL has dividend account in Southeast Bank Limited through this account BPBL pays dividend to the shareholders. Generally BPBL pays dividend of that year in March or April of the following year.

Interpretation:

BPBL distributed 40.51%, 28.00%, 49.36%, 57.88% and 55.45% of its net income as dividends in 2008,2009,2020, 2022 and 2013 respectively and retained the remaining as retained earnings for other operating and investment needs and the ratio gradually increases. BPBLs dividend payout ratio is healthy which leads to investor confidence in the company. So BPBLs stable dividend payout ratio indicates a solid dividend policy by the company’s board of directors.

Short term Liability Management:

Sometimes BPBL requires short term loan from private commercial banks. Generally BPBL takes overdraft loan from SCBL, CITI N/A, HSBC and CBCL. The reasons being the following:

- To make payments to the suppliers

- To meet the dividend payment requirements

- To make L/C payment

- To manage working capital needs and

- To make salary payment

Analyzing and calculating financial expense: BPBL has some short term loans in CBCL, SCBL, HSBC and CITI N/A. In case of emergency BPBL borrows money from those banks against its overdraft limit. So, another important task of treasury department is to analyze and calculate financial expense of those loans. To calculate and analyze financial expenses; concerned officer needs following information:

- Amount of overdraft or loan

- Interest Rate

- Period of the overdraft or loan

- The interest rate is compound or simple interest

Observation:

The chart and table shows the financial expensed or borrowing costs of last five years of BPBL. The trend of financial expenses highly fluctuated from 2009 to 2012 and 2013 it reduced by 78.68% and 59.08% which were better for BPBL. But in 2011 financial expenses of BPBL massively increased. Because of high bank interest rate in 2011, the financial expense in 2011 was high. It might also happen for borrowing more or inefficiency of cash management.

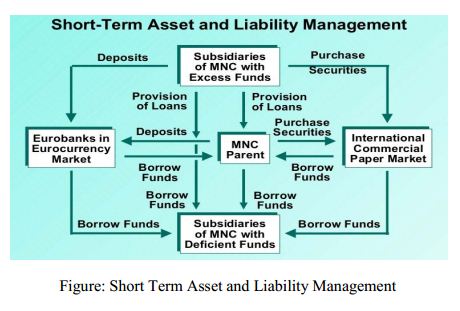

Short Term Investment:

BPBL sometime has surplus fund or idle cash; it does not provide any return for the firm, if it is invested it can generate some return for the shareholders, so treasury management has to take short-term investment decision. Short-term investment process has following steps:

- Check or forecast surplus fund or idle cash fund

- Request and recommend investment

- Approve investment request

- Receive and compare offer letter which was obtained from investment firms or financial institutions

- Analyze and evaluate the investment proposal

- Select investment firms and accept the proposal

- Approve the investment

- Sign the agreement with selected financial institutions and archive the documents.

Analyzing and calculating accrued interest income of short-term investment: BPBL has some short-term investments in Treasury bill of Bangladesh bank, fixed or term deposit in ULCL, Prime bank Ltd and Mutual trust bank ltd and investment under countervailing lease agreement with IDLC. So, another task of treasury department is to analyze and calculate the accrued interest amount on maturity date of those investments. To calculate and analyze accrued interest; concerned officer needs following information:

- Amount of FDR or TD or Lease amount

- Interest rate

- Maturity period and date

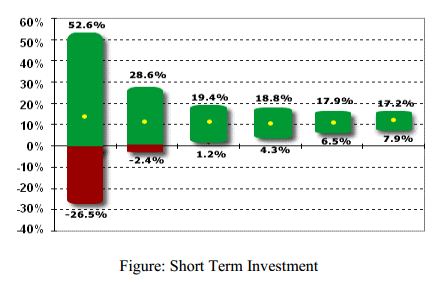

Observation:

The chart and table shows the interest income on FDR, STD and Treasury bill of last five years of BPBL. The trend of interest income highly fluctuated from 2009 to 2012.In 2009 it increased by 48.32% than 2008 and in 2010 massively increased by 209.82% than 2009 which generated more interest income or profit for BPBL from surplus cash. But in 2011 interest income on FDR, STD and Treasury bill reduced by 62.222% compared to 2010 and in 2012 it were insignificantly reduced. Many causes were behind for high interest income in 2010 such as investment

institutions might provide high interest rate on investment or large amount of investment by BPBL or BPBL cash department choose right decision on right time. On the other hand, in 2011 to 2013 BPBLs cash department could not retain the success of previous two years but BPBL had more cash in hand than 2009 and 2010, it might be a failure and inefficiency of cash forecasting and cash management.

Findings:

After conducting the report through various analysis and evaluation of treasury procedure, many findings has been found, it includes both positive and negative findings. The function of treasury department of BPBL is distinguished and certain. Treasury department has sound standard operating procedures for accomplishing every task. BPBL has an efficient and effective distribution strategy. BPBLs collection of sales proceeds system and fund disbursement system are convenient for both customer and suppliers. For effective fund collection system the last three years cash collection performance was excellent and it take low processing time to collect fund. For efficient liquidity management Treasury department is able to make payment to its creditor as early as possible. L/C opening and settlement system of BPBL is a convenient and sound process of BPBL makes purchase fund at low cost or low exchange rate. BPBLs stable dividend payout ratio indicates a solid dividend policy by the company’s board of directors.

BPBL has strong and good liquidity position and had no opportunity to run out from short-term financial solvency and this ability rises gradually (Current/Quick/Cash).BPBLs most of debts consist of creditors and accrual so BPBLs borrowing cost is insignificant. As a result BPBL is in good position regarding borrowed money compared to the resources invested by the shareholders (Debt to equity ratio).BPBLs asset-liability management efficiency increased day by day. BPBL is the less leveraged company and it has lower financial risk (Total Debt Ratio).The company is

also able to use its assets and equity efficiently and effectively. The company increases its sales through inventory control and was efficiently managing and selling its inventory so BPBL tied up the fewer funds.

The gross profit margin ratio is highly satisfactory and ROA shows that BPBL is more profitable. The EPS had a gradual increase trend which is a good profitability indicator of BPBL. Berger’s profit after tax has a clear indication of its financial viability. ROE under Du-Pont analysis of BPBL indicates operating efficiency, asset use efficiency and financial leverage of BPBL is reliable. Finally BPBL is showing an upward trend in every aspect of financial statements.

Besides above positive aspects of BPBL, the following problems of limitations have been found-

1. Since BPBL deals with multiple banks, it may get difficult to know the true cash standings for lack of internal controls and information gap among the various department, sales offices and BPBLs financial partners. BPBL selected Citi Bank N/A for sales proceeds collection, which has no branch in remote area in Bangladesh, So it may create problem for treasury department in collection process and as well as BPBL customer cannot easily deposit money into bank; it ultimately increases collection time and this keeps negative impact on cash management

2. BPBL does not keep safety cash balance for unanticipated cash demand. BPBLs fund disbursement or payment process has lack of synchronization among various department and suppliers.

3. Lack of team work and manpower in treasury department of BPBL because TM has a lot of activities and it is tough to maintain communication and accomplishing tasks with a lot of financial partners by few manpower.

4. Lack of financial electronic data interchange (FEDI) system through which financial information and fund is transferred.

5. Lack of Pre-authorized payment arrangement for cash collection and disbursement.

6. BPBL has no backward integrated firm for producing raw materials for itself.

7. BPBLs inventory holdings days are too much high. In average it was found that inventory holdings days were 95.2 days in the last five years which is delaying into converted cash from inventory and it creates liquidity problems in BPBL but BPBL plays its suppliers and other creditors so fast.

8. For information gap and wrong check number input by sales officers, it tough and confused to reconcile bank account and identify wrong entry in cash book or bank book.

9. Treasury department does not have any tools for foreign exchange rate and interest rate risk forecasting and lack of prediction of foreign exchange rate to take advantage from currency speculation in its LC operation. Low integration between treasury department and supply chain department which creates puzzles in LC operation and others third party payment

10. Treasury department has also inefficacy in short term investment because the interest income fell in 2011 and 2012 but BPBL had more cash in hand in those two days. BPBL does not make any investment in marketable securities to foster the idle cash management inefficiency in using cash and other short-term assets.

Recommendation:

According to the summary of limitations or problems the followings are recommendations for overcoming or correcting errors and improving BPBLs treasury management process as well as for BPBL profitability growth:

1. BPBL needs to make sure that they have a clear view of the true cash position at any point of time. Since they deal with multiple banks, it may get difficult to know the true cash standings. For this purpose they need to have better internal controls so that the flow of information among all the departments is smooth. BPBL and its bankers should drive for the convergence towards electronic payments and collections to better integrate money and information flows. This will help the treasurers to exactly determine the cash position of the company on the real time basis.

The other areas in which cash has to be efficiently managed include:

- Explore centralizing cash and treasury management

- Ensure that treasury and cash management systems are up to date

- BPBL should maintain a collection account, a bank which have branch not only in urban area but also in remote area.

- Treasury department should retain success of collection of fund and try to reduce collection delay and processing time more.

- BPBL should increase online collaboration with banks to create effective relationship between its financial partners.

2. BPBL needs to have better visibility of the cash standing so that they can effectively disburse their surpluses and deal with negative cash balances. An obvious place to start is to sweep any surpluses into deposit accounts or investing in short-term money markets. Where loans exist or accounts are overdrawn, cash can be more productively used to offset these, thus minimizing interest payments.

3. Treasury Department should increase financial electronic data interchange system to eliminate paper or invoice which is increase efficiency in treasury management and support to file management and task can be done promptly.

4. Treasury department should maintain safety cash balance to meet unanticipated demands of cash and keep safety foreign currency to open LC and minimize the exchange rate risk.

5. The current assets should be managed more effectively so to avoid unnecessary blocking of capital that can be used for other purposes.

6. BPBL should increase efficiency in inventory management. Company should reduce inventory holding days with use of Zero inventory concepts for reducing or warehousing cost by bringing efficiency in sales and marketing activities.

7. BPBL tries to maintain profit after tax growth rate at the same growth rate of turnover. BPBLs operating profit margin was highly reduced from gross profit margin, so BPBL should concern on reducing high administrative and selling expense efficiently.

8. BPBL need to take initiative to introduce backward integrated firm for producing raw materials to take cost advantage.

Conclusion:

Treasury management is increasingly assuming more strategic roles in companies. Thus, it is a challenge for the treasury department to continue making effective and efficient management of collection and disbursement of cash flow. Finally it was observed that, the treasury management procedure of BPBL is a sound, effective an efficient process. The report evaluates the collection and disbursement process, cash management, short-term liability and investment management through ratio analysis and other tools. The report also examines the company financial

performance. The various ratios calculated are an indicator as to the fact that the profitability of the firm are on a rise. It is really a challenge for BPBL to retain success in financial performance, profitability growth and competitive advantage.

It was a great opportunity for me to work with one of the leading company of Bangladesh. My aim was to understand treasury management procedure of Berger Paints Bangladesh Limited through analyzing and evaluating treasury functions. Bank Reconciliation, Foreign Exchange Rate Forecasting and Settlement, Calculation and analyzing the bill of daily/Monthly sales, Annual Forecasting and the most important SAP (System Applications and Products in Data Processing) in treasury department was the part of my learning’s.