A voluntary foreclosure is a foreclosure action taken by a borrower who is unable to make loan payments on a property and wants to avoid involuntary foreclosure and eviction. The borrower enthusiastically enters dispossession since they can’t make advance installments, or they wish to try not to make any future installments. The borrower relinquishes possession of the property to the lender. If a borrower’s mortgage is considerably underwater, they may pick this alternative.

On the off chance that the borrower battles to make installments or tries not to make installments through and through, a compulsory dispossession will follow. The dispossession is started by the moneylender to hold onto ownership of the property, potentially prompting ousting for the borrower. This is distinct from an involuntary foreclosure, which is undertaken by the lending institution in order to seize a property in order to recoup the lender’s losses and is often the last resort for debtors who are unable to make loan payments.

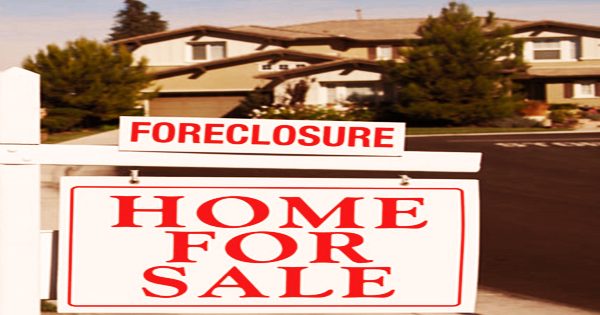

On the off chance that compulsory dispossession and expulsion appear to be unavoidable, an intentional abandonment is regularly the better alternative for the borrower. They can leave the property according to their own preferences and end their advance installments sooner. For both residential and commercial properties, borrowers can request a voluntary foreclosure from a bank or other lending institution. Strategic default, walking away, jingle letter, and amicable foreclosure are all expressions that can be used to describe voluntary foreclosures.

When a homeowner is no longer able or willing to make mortgage payments on the debt that was used to finance the property, a voluntary foreclosure occurs. It tends to be destructive to a borrower’s credit scores, however it is generally not as monetarily harming as a compulsory abandonment. Responsibility for property is moved from the borrower to the bank in return for delivering the borrower from installment commitments. The late-2000s subprime mortgage crisis, when many mortgages were underwater, resulted in a huge increase in voluntary foreclosures.

Foreclosure might have a negative impact on a borrower’s ability to find work. Voluntary foreclosure is severely destructive to a borrower’s credit report and can make renting or buying a home and getting loans authorized difficult for years thereafter, but it is not as financially ruinous as an involuntary foreclosure. All things considered; it is more ideal than a compulsory dispossession. Settling on an intentional dispossession will essentially moderate the harm.

Friendly foreclosures, mortgage discharge, walking away, and strategic default are all terms used to describe voluntary foreclosures. During the Great Recession, voluntary foreclosures became very popular. With the American lodging bubble and subprime contracts, borrowers battled to make installments on their home loans. They acquired too far in the red, and the downturn left numerous jobless, which exacerbated the monetary strain contract installments caused.

Before their credit rating declines, many debtors prepare for a voluntary foreclosure by obtaining new credit cards and taking out new vehicle loans and mortgages. In addition to the challenging circumstances, property prices plunged, and many mortgages became underwater, meaning that homeowners owed more than the home was worth. Moneylenders will regularly consent to a borrower’s solicitation for deliberate dispossession since it can make the way toward retaking property and gathering obligations a lot quicker and savvier than a compulsory abandonment.

A deed in lieu of foreclosure is a document that is used in the majority of voluntary foreclosures. In exchange for the borrower’s release from payment obligations, the deed will transfer ownership of the property from the borrower to the lender. The principles, laws, and punishments for willful dispossessions fluctuate broadly by loaning establishment and state. Utilizing the interaction with the deed in lieu of dispossession stays away from an expensive and tedious standard abandonment. It benefits both the lender and the borrower.

Pros and Cons of Voluntary Foreclosure:

Pros of Voluntary Foreclosure –

- Ends payments sooner: A voluntary foreclosure is a borrower’s last resort, yet it might be the shortest way to relief. It is substantially quicker than a traditional foreclosure. Furthermore, because this foreclosure is initiated by the borrower, the borrower has complete control over whether or not they can or will make payments at any time.

- Option to leave on own terms: It’s far preferable to leave on your own terms than to be forcibly evicted due to an involuntary foreclosure. When a borrower opts for a voluntary foreclosure, they are free to decide their next steps. It alleviates one of the most stressful aspects of the foreclosure process; figuring out where you’ll live next.

- Less credit impact than involuntary foreclosure: A voluntary foreclosure has less impact on your credit than an involuntary foreclosure. It is well known that using a deed in lieu of foreclosure softens the credit impact and shortens the duration of the impact. Involuntary foreclosures can damage credit for up to seven years, whereas a deed in lieu of foreclosure can have a four-year impact.

- Faster and easier process for lenders: A voluntary foreclosure, as opposed to an involuntary foreclosure, can be a win-win situation for both the borrower and the lender. For both parties, the process is speedier and less inconvenient.

Cons of a Voluntary Foreclosure –

- Credit is still severely impacted: While a voluntary foreclosure has a lower credit impact, it can still be disastrous. Your credit score will drop, causing a cascading effect that will have significant ramifications.

- Housing and employment issues: Housing and employment concerns are two of the repercussions. Your credit score has an impact on the type of housing you can get and the interest rates you’ll pay on any future mortgages. That is, if you are successful in getting accepted. If a lender learns that you have previously voluntarily foreclosed, they may refuse to lend to you. It will present challenges that you must solve in order to obtain a roof over your head. Credit records of candidates who are being considered for employment can now be checked by employers. It’s a precautionary measure, but it can reveal information about you as a borrower and how you’d perform as an employee. This is especially true if the job entails money management. A poor credit score can be a warning sign.

- Deficiency judgment: A voluntary foreclosure can potentially result in a deficiency judgment. The alleviation of 100% of a borrower’s debt is typical, but it is not guaranteed. The borrower may be responsible for the difference between the home’s value and the mortgage debt. They could be held accountable for the entire discrepancy or only a fraction of it. It would be a financial hardship in either case. When a borrower initiates a voluntary foreclosure with a lender, they should be aware of the terms.

- Potential taxes owed for debt relief: If a deficiency is forgiven, the forgiven debt may have tax ramifications. The IRS considers debt cancellation to be taxable income. So, while a debt may be forgiven, it may be accompanied with a tax bill. Owing assessments on the obligation is a lot simpler to pay off than the actual obligation, however the expense bill can in any case be exorbitant and hard to pay when a borrower is tight on cash.

Voluntary foreclosures more than doubled from 2007 to 2008, according to some figures, and accounted for more than 25% of all defaults in 2009. Home values have not grown sufficiently to liberate many debtors from the burden of negative equity, therefore voluntary foreclosures have remained widespread during the last decade.

Information Sources: