Introduction:

Bangladesh is one of the largest Muslim Countries in the world. The people of this country are deeply committed to lead an Islamic way of life which is based on the principle of Holy Quran and the Sunah. The Al-Arafah Islami Bank which is established on June 18, 1995 is the true reflection of this inner urge of its people which started functioning with effect from September 27, 1995. It is committed to conduct all Financial Activities banking and Investment activities on the basis of interest free profit and loss sharing system. In doing so it has unveiled a new horizon and unheard in new silver lining of hope towards materializing a long cherished dream of the people Bangladesh for doing their Banking transaction in line with what is prescribed by Islam. With the active cooperation and participation of Islamic Development Bank (IDB) and some other Islamic Banks, financial institutions and government bodies, Al-Arafah Islami Bank Limited has new earned the unique position of a leading private commercial bank in Bangladesh. Al-Arafah Isalmi Bank Limited has made a positive contribution towards the socio economic development of the country by opening 46 branches in which 16 authorized dealer throughout the county.

The equity of the bank stood at Tk. 1690 Million Cr. As on 31 December 2010 .The manpower was 912 and the number of shareholders was 4487. During my 3 months Internship of Al-Arafah Islami Bank Limited, the experiences that I learned are expressed in my report.

Purpose of the Report

The student of BBA program of Northern University Bangladesh is required to undergo an internship program at the end of final semester. As a part of the program, I was been placed in Al-Arafah Islami Bank Ltd. for a period of three months. From this perspective, on completion of three months internship program, I have prepared this report. I truly appreciate this assignment and do hope that it will be a great importance in building my future carrier.

Objectives of the Report

General Objective of the Report:

The main purpose of the study to know the overall financial operational performance of the Al-Arafah Islami Bank Ltd. and fulfilling the practical requirements of the BBA program . The objective of Islamic banking is not only to earn profit but also to do good and welfare to the people. Islam upholds the concept that money, income and property belong to Allah and this wealth is to be used for the God of the society.

Specific Objectives are:

- To have a practical relation & reliability of the topics we have achieved from textual background in our educational life.

- To develop understanding of Business Communication application in practical field.

- To develop our capabilities as an employee in realistic field of the job market.

- To improve corresponding, report writing ability.

- Presentation of an introduction to the organization Al Arafah Islami Bank Ltd. as a whole.

- To familiarize with practical job environment.

- To have an exposure on the financial institutions such as banking environment of Bangladesh.

- To gain experience on different functions of the different departments of the bank.

- To observe banker-customer relationship.

- To relate the theories of banking with the practical in banking

Scope of the Report

As I was working in the Al-Arafah Islami Bank Limited, Motijheel Branch, I got the opportunity to learn different part of banking system. My supervisor divided the whole banking in three parts so that I can get the opportunity to work in both the divisions, General Banking division Investment division and Foreign Exchange division to analysis the whole financial activities.

METHODOLOGY:

To make the report more meaningful and presentable, two sources of data and information have been used widely these are Primary Data and Secondary Data. Both primary and secondary data sources were used to generate the report. But Most of the information collected from secondary sources:

Secondary Sources: The secondary sources of information is:

- Annual report of AIBL.

- Materials and files of AIBL, Foreign Exchange Branch.

- Website of AIBL.

- Unpublished data received from the branch.

- General information of banking activities.

Primary sources: The primary source of information is as follows:

- Face-to-face conversation with the bank officers and staffs.

- Practical desk work

- Personal diary (that contains every day experience in bank while under going practical orientation)

Limitation

The work is mainly based on interpreting primary data. There is insufficiency of Secondary data, but for the purpose of the betterment of the present position of the bank’s accounting procedure, collecting, interpreting and integrating primary data has been utilized.

Though a very comprehensive and a well-organized report has been tried to be produced but there are still some limitations present here.

Since the time allocated for internship program is twelve weeks, it may have a coercive effect on this study lowering the actual value and standard.

- The communication gap among the different personnel because of excessive workload.

- Inexperience about practical work.

- Because of sensitiveness, the department does not want to disclose information about the financial situation, which leads to do report.

- Lack of accessibility to respondents.

- The bank authorities are so busy that they could not give me sufficient time for discussion about Accounting Procedure and its problems.

- Dealing with some ambivalent information.

- Problems for lack of my research work

- Clients are not always interested to spend time for interviews.

- The main constraint was insufficiency of information, which is highly required for the study. It was unable to provide some formatted documents and data for the study.

- Since the bank personnel were very busy, they failed to give me enough time to complete the report.

- The clients were very busy. So, they were unable to give me much time for interview.

- Such a study carried out by me for the first time. So, inexperience is one of the main factors that constituted the limitation of the study.

Historical Background of AIBL

Islam provides us a complete lifestyle. Main objective of Islam lifestyle is to be successful both in our mortal and immortal life. Therefore in every aspect of our life we should follow the doctrine of Al-Quran and lifestyle of Hazrat Muhammad (sm) for our supreme success. Al-Arafah Islami Bank started its journey in 1995 with the said principles in mind and to introduce a modern banking system based on Al-Quran and Sunnah.

A group of established, dedicated and pious personalities of Bangladesh are the architects and directors of the Bank. Among them a noted Islamic scholar, economist, writer and ex-bureau craft of Bangladesh government Mr. A.Z.M. Shamsul Alam is the founder Chairman of the bank. His progressive leadership and continuous inspiration provided a boost for the bank in getting a foothold in the financial market of Bangladesh.

A group of 26 dedicated and noted Islamic personalities of Bangladesh are the member of executive council of the bank. They are also noted for their business acumen. Al-Arafah Islami Bank Ltd. Has 79 branches.

Wisdom of the directors, Islamic bankers and the wish of Almighty Allah make Al-Arafah Islami Bank Ltd. most modern and a leading bank in Bangladesh.

Objective of AIBL:

Al-Arafah Islami Bank Limited is Islamic Banking institutions that operates with the objectives implement and materialize the economic and financial principles of Islamic in the banking arena. The objectives of AIBL are not only to earn profit, but also to do good and welfare to the people. The main objectives of AIBL are listed below-

- To establish participatory banking instead of banking on debtor creditor relationship

- To invest through different modes permitted under Islamic Shariah

- To accepts deposits on profit loss sharing basis

- To establish as welfare-oriented banking system

- To extend co-operation to the poor, the helpless and the low income group for their economic up liftmen

- To play a vital role in human development and employment generation

- To contribute towards balances growth and development of the country through investment operations particularly in the less developed areas

- To contribute in achieving the ultimate goal of Islamic economic system

- To conduct interest free banking

Special feature of AIBL:

- All activities are conducted and interest free system according to the Islamic shariah

- Its investment policies under different modes are fully shariah complain

- During the year2009, 70% of the investment income has been distributed among the Mudaraba depositors

- It believes in providing dedicated services to the clients imbued with Islamic spirit of brotherhood, peace and fraternity.

- The bank is committed towards establishing welfare oriented banking system to meet the needs of low income and underprivileged class of people.

- The bank upholds the Islamic values of establishment of just economic system through social emancipation and equitable distribution of wealth.

Financial Information about AIBL:

| Particulars | 2010 | 2009 | 2008 |

| Investment income | 3502.14 | 2243.15 | 1742.19 |

| Profit paid to depositors | 2220.47 | 1628.63 | 1245.12 |

| Net investment income | 1281.68 | 614.52 | 480.52 |

| Commission, Exchange and other income | 885.12 | 712.46 | 510.12 |

| Total operating income | 2166.80 | 1326.98 | 1045.12 |

| Total operating expense | 638.70 | 570.80 | 470.58 |

| Profit before tax and provision | 1528.10 | 756.18 | 578.45 |

| Provision on investment and others | 269.20 | 173.34 | 115.12 |

| Profit before Tax | 1258.90 | 582.84 | 480.23 |

| Net profit after Tax | 668.24 | 347.31 | 250.58 |

| Earning per share(EPS) | 148.29 | 25.10 | 15.10 |

Mission of AIBL:

- Achieving the satisfaction of Almighty Allah both here& hereafter

- Proliferation of Shariah Based Banking practices

- Quality financial services adopting the latest technology

- Fast and efficient customer service

- Maintaining high standard of business ethics

- Balanced growth

- Steady& competitive return on shareholders equity

- Innovative banking at a competitive price

- Attract and retain quality human resources

- Extending commitment to the growth of national economy

- Involving more in Micro and SME financing

Vision of AIBL:

- To operate based on Islamic principles of transactions along with ensuring justice and equity in the economy.

- To be a pioneer in Islami Banking in Bangladesh and contribute significantly to the growth of the national economy

- To improve Banker customer relationship through improving customer service

- To develop now and innovate product/service through integration of technology and policy and principle

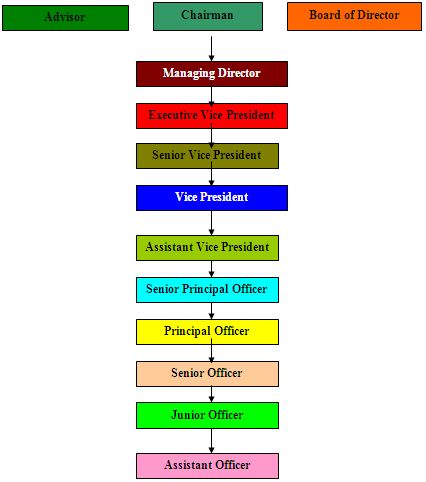

Organ gram of Al-Arafah Islami Bank Ltd.:

Financial Performance of Al- Arafah Islami Bank Ltd.:

AIBL is one of the now entrants of the 3rd generation banks having only 79 branches currently. With in short time period, AIBL has been to create an image as a progressive and dynamic financial institution for itself and has earned significant reputation in the country banking sector. Despite of stiff competition in banking sector, AIBL witness a considerable improvement in its overall business performance during 31 December, which contributed to consolidate the position of the bank. At the end of current year, the number of depositors stood at 243273 and the amount deposi8t has accumulated to TK.16775.33 million. The total numbers investors are 13213 and total investment extended to them was a sum of taka 17423.19 million.

The bank has earned TK.2172.48 million and i8ncurred an expense of TK.1202.71 million in the current year. At the end of the year the profit before tax has stood TK.855.47 million, which is 78.97% more than TK.478.00 million pre-tax income of the last year.

Modes of Investment:

1. Bai-Murabaha:

Bai-Murabaha may be define as a contract between a buyer and a seller under which the seller sells certain specific goods (permissible under Islamic Shariah and the law of the land ) to buyer at a cost plus agreed profit payable in cash or on any fixed future date in lump sum or by installments. The profit marked up may be fixed in lump sum or in percentage of the cost price of the goods.2. Mudaraba:

Moradabad refers to a contract between two parties in which one party supplies capital to the other party for the carrying on some trade on the condition that the resulting profits are distributed in a mutually agreed proportion and loss is borne by the provider of the capital.

3. Musharaka:

The word ‘musharaka’ is derived from the Arabic word ‘Sharikah’. That means partnership. It is a partnership between two or more parties who trade woth a join capital. The profit is to be dividends into a known and fixed percentage. All the partners including the bank have the right to participate in the management.

4. Bai-Muajjal :

A contract in which the seller allows the buyer to pay the price of a commodity at a future date in lamp sum or installment (which may be higher than the spot price) this is a sort of credit sale for profit. Bai-muajjal is useful in financing requirements of industry and agriculture.

5. Bai- Salam:

Bai-Salam is a contract in which the buyer pays the agreed price of a commodity in advance and the commodity is delivered to the buyer at a specified future price. This is useful mechanism for agricultural products and industrial product.

Risk management

The risk of Al-Arafah Islami Bank limited is defined as the possibility of losses, financial or otherwise. The risk management of the Bank covers 6 (six) Core risk Areas of banking .Credit risk management, foreign exchange risk management, Assets Liability Management, prevention of money laundering and establishment of Internal control and Compliance and information & communication technology. The prime objective of the risk management is that the Bank takes well calculative business risk while safeguarding the Banks capital, its financial resources and profitability from various risks. In this context, the Bank took steps to implement the guidelines of Bangladesh Bank as under.

Credit risk management:

Credit risk is one of the major risks faced by the Bank. This can be descried a potential loss arising from the failure of a century party to perform as per contractual agreement with the Bank. The failure may result from unwillingness of the counter party of decline in his/her financial condition. Therefore, Banks credit risk management activities have been designed to address all these issues. The bank has segregated the Investment Risk management committee at Head Office. The committee reviews the Investment risk issues on monthly basis. The bank has segregated the Investment Approval, Investment Administration, Investment Recovery and Legal Authority. The Bank has segregated duties of the officers/executives involved in credit related activities. A separate Business Development Department has been established at Head Office, which is entrusted with the duties of maintaining effective relationship whit the customer, marketing of credit products, exploring now business opportunities etc. In the branches of the bank separate officials are engaged as Relationship

Manager, Documentation Officer, Verification Officer, disbursement Officer and Recovery Officer. Their jobs have been allocated and responsibilities have been defined.

Foreign Exchange Section:

In the motojheel branch, I worked mainly in this section. I prepared several voucher for foreign remittance. Different types of remittance come from different countries. In motijheel branch, remittance is an important section. Every day huge remittance comes from several countries. Besides I prepared import file. Every month AIBL have to submit the import, export and remittance file to the Bangladesh Bank.

I have done the following important tasks along with the prudent employees

- Opening and payment settlement of L/C

- Insurance of shipping guarantee

- Advising L/C

- Preparation of daily and weekly statement

- Voucher making or issuing

- Amendment of L/C and register maintaining

Learning points:

I have learnt so many operations abut the banking sectors especially IBBL banking sector. The following statement that I have learnt and that is given below

- How to open several types of accounts

- What are the requirements for opening different types of account?

- How clients can gather their account statement and know the balances.

- What are the procedures to close an account?

- How to collect the new cheque.

- How foreign exchange section operates their operation.

- How foreign remittance for outward

- How clearing house operates their operation.

- I have learnt about several types of investment modes of AIBL.

- How to collect foreign remittance and how do they reach to clients.

- How to open Letter of Credit

- How to import process

- How to export process

- I have learnt a systematic life through internship period

- How to deal with customer

- I have learnt about TT, DD and PO

- How each section of the branch provides the services to their clients?

- How to collect cheque from clients for cle

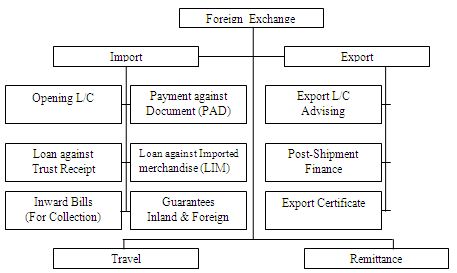

Foreign exchange department

Following flow chart depicts the multifarious functions usually done by the FED:

Foreign exchange can simply be defined as a process of conversion of one currency into another. In ordinary sense “Foreign Exchange” means Foreign Currency, which refers to the rate of exchange the price of one unit of foreign exchange in terms of another currency. But in its complete sense, foreign exchange means the mechanism or the media used and the rate at which these media are exchange with another.

Foreign Exchange department of Al-Arafah Islami Bank Ltd. is one of the most important of all departments. This department divided into three parts, the first one is the Import Department the second part is the Export Department & the third part is Foreign Remittance Department.

Import Procedure

To import a person should be competent to be an “Importer”. According to Import and Export control Act 1950, the office of Chief Controller of Import and Export provides the registration (IRC) to the importer. After obtaining this person has to secure a letter of credit authorization from Bangladesh Bank. And then a person becomes a qualified importer. He is the person who requests or instructs to open an L/C. he is also called opener or applicant of the credit.

Importer’s Application for L/C Limit Margin

To have an import L/C limit, an importer submits an application to the Department of Al-Arafah Islami Bank Ltd. furnishing the following information:

1 Full particulars of bank account.

2 Nature of business.

3 Required amount of limit.

4 Payment terms and conditions.

5 Goods to be imported.

6 Offered security.

7 Repayment schedule.

Now if the officer thinks the application to open an L/C in not fit, the following entries are given to realize the L/C, Charges, Postage and L/C margin.

Bill of exchange

A Bill of Exchange is an instruction by the exporter (drawer) to the importer or the importer’s bank to make payment of the amount mentioned in it. A Bill of Exchange is a negotiable instrument and is governed by the Negotiable Instruments Act. The bill under a letter of credit may be drawn in the issuing bank or another drawee bank but not on the importer. If the credit nevertheless calls for a bill on the applicant, the bank will consider such bills as additional documents. The various types of bills are:

D/A and D/P bills

A usance bill may be on D/A or D/P terms. If it is on D/a terms (Documents against acceptance), the collecting bank is to deliver the documents to the drawee on the acceptance of the bill by him. The payment will be made by the drawee on the due date of the bill. For the period from the date of acceptance to the date of payment, the bank remains unsecured. If it is a D/P bill (Documents against payment), the documents will be delivered to the drawee only on payment until which time they are retained by the bank. Therefore, the bank retains control over goods until payment is received.

Inland and foreign bills

A bill, which is drawn in Bangladesh and made payable in or drawn upon any person resident in Bangladesh, is an inland bill. Thus, an inland bill must fulfill both the conditions that (i) it is drawn in Bangladesh and (ii) it is payable in Bangladesh or drawn on person resident in Bangladesh (even though payable abroad). Any bill that does not fulfill either of the conditions is a foreign bill. Thus, a bill drawn in Bangladesh, payable at a place outside Bangladesh by a person resident outside Bangladesh and a bill drawn at a place outside Bangladesh, but payable in Bangladesh are foreign bills.

Marine Insurance Policy

The loss or damage to goods during the voyage or shipment would affect any one or more parties involved in the transaction, viz., the importer, the exporter, the shipping company and the bank which has paid against the documents covering the goods. Marine insurance offers the desired cover against loss of or damage to the goods during the transaction. It allows free flow of international trade by absorbing an important uncertainty connected with it.

Marine insurance may cover the ship (hull insurance) or the goods (cargo insurance). The consideration for which a marine insurance contract is undertaken is the ‘premium’. The insurance may be for either partial loss or total loss. The applicant must submit the insurance cover note and the money receipt with other relevant documents to the advising bank.

Invoices

Various types of invoices are required in L/C. Brief descriptions of those invoices are given below:

Commercial Invoice

A commercial invoice is a statement containing full details of the goods sipped. The general contents of a commercial invoice used in foreign trade are:

- Names and addresses of the seller and buyer;

- Details of goods shipped-quantity, quality, description and value;

- Packing details and packing marks;

- Price and amount payable by the buyer;

- Terms of trade-FOB, CFR OR CIF, etc;

- Details of freight charges, insurance premia and other chargers;

- Reference to the sale contract in fulfillment of which the shipment is made;

- Name of the vessel in which the goods are shipped; and

- Reference to the license number under which the import is made.

Export Procedure

Entering into an Export contract

In order to avoid disputes, it is necessary to enter into an export contract with the overseas buyer. For this purpose, export contract should be carefully drafted incorporating comprehensive but in precise terms, all relevant and important conditions of the trade deal.

There should not be any ambiguity regarding the exact specifications of goods and terms of sale including export price, mode of payment, storage and distribution methods, type of packaging, port of shipment, delivery schedule etc. The different aspects of an export contract are enumerated as under :

- Product, Standards and Specifications

- Quantity

- Inspection

- Total Value of Contract

- Terms of Delivery

- Taxes, Duties and Charges

- Period of Delivery/Shipment

- Packing, Labeling and Marking

- Terms of Payment– Amount/Mode & Currency

- Discounts and Commissions

- Licenses and Permits

- Insurance

- Documentary Requirements

- Guarantee

- Force Majeure of Excuse for Non-performance of contract

- Remedies

Arbitration It will not be out of place to mention here the importance of arbitration clause in an export contract Court proceedings do not offer a satisfactory method for settlement of commercial disputes, as they involve inevitable delays, costs and technicalities. On the other hand, arbitration provides an economic, expeditious and informal remedy for settlement of commercial disputes. Arbitration proceedings are conducted in privacy and the awards are kept confidential. The Arbitrator is usually an expert in the subject matter of the dispute. The dates for arbitration meetings are fixed with the convenience of all concerned. Thus, arbitration is the most suitable way for settlements of commercial disputes and it may invariably be used by businessmen in their commercial dealings.

Export Pricing and Costing

Export pricing should be differentiated from export costing. Price is what we offer to the customer.Cost is the price that we pay/incur for the product. Price includes our profit margin, cost includes only expenses we have incurred. Export pricing is the most important tool for promoting sales and facing international competition. The price has to be realistically worked out taking into consideration all export benefits and expenses. However, there is no fixed formula for successful export pricing. It will differ from exporter to exporter depending upon whether the exporter is a merchant exporter or a manufacturer exporter or exporting through a canalising agency. You should also assess the strength of your competitor and anticipate the move of the competitor in the market. Pricing strategies will depend on various circumstantial situations. You can still be competitive with higher prices but with better delivery package or other advantages.

Your prices will be determined by the following factors:

- Range of products offered

- Prompt deliveries and continuity in supply

- After-sales service in products like machine tools, consumer durables

- Product differentiation and brand image

- Frequency of purchase

- Presumed relationship between quality and price

- Specialty value goods and gift items

- Credit offered

- Preference or prejudice for products originating from a particular source

- Aggressive marketing and sales promotion

- Prompt acceptance and settlement of claims

- Unique value goods and gift items

The exports form Bangladesh is subject to export trade control exercise by the Ministry of Commerce through Chief Controller of Export and Imports (CCI & E). No exporter is allowed to export any commodity permissible for export from Bangladesh unless he is registered with CCI & E and holds valid Export Registration Certificate (ERC). The Export Registration Certificate (ERC) is required to be renewed every year. The Export Registration Certificate (ERC) is to be incorporated on EXP forms and other documents connected with exports.

Papers Requirement for new Export

- Export Realization Certificate (ERC).

- Trade License.

- Membership Certificate Form Chamber/ EPB.

- Account To Be Maintained With Bank.

- Export L/C Contract.

- EXP Form To Be Certified.

- TIN Certificate.

- VAT Certificate.

- Memorandum and Article of Association of the Company.

- Confident Credit Report to Be Obtained of the Importer.

- Registered Partnership Deed In Case of Partnership Concern.

Preparation of Exports Documents

- Bill of exchange or Draft.

- Bill of Lading.

- Invoice.

- Insurance Policy/ Certificate.

- Certificate of Origin.

- Inspection Certificate.

- Consular Invoice.

- Packing List.

- Quality Control Certificate.

- GSP Certificate.

- Photocopy-sanitary Certificate.

Export Financing

- Export Cash Credit (ECC).

- Packing Credit (PC)

- Back-to-Back Credit Facility (BTB).

- Foreign Documentary Bills Purchased (FDBP).

Processing and Opening of Back-to-Back Letter of Credit

An exporter desired to have an Import L/C limit under Back-to-Back arrangement. In that case the following papers & documents are required:

- Full Particulars of Bank Account.

- Balance Sheet.

- Statement of Assets & Liability.

- Trade License.

- Valid Bonded Warehouse License.

- Membership Certificate.

- Income Tax Declaration.

- Memorandum of Articles.

- Partnership Deed.

- Resolution.

- Photographs of Al Directors.

On receipt of above documents and papers the Back-to-Back Letter of Credit opening section will prepare a credit report. Branch must obtain sanction from Head Office for Opening Back to Back L/C.

Back-to-Back Letter of Credit opened without Head Office concern because of valued clients of the Bank. In that case an officer of Foreign Exchange Department will send a Post to the Head Office for the opened Back-to-Back Letter of Credit

Export Cash Credit (ECC)

Export Cash Credit (ECC) is extended to the companies who are involved in exporting goods and services. Export Cash Credit (ECC) is provided to procure raw materials, Packing List, Wages, Salaries, Utility etc. the quantum of Export Cash Credit (ECC) is usually 75% of the export L/C.

Packing Credit (PC)

Packing Credit (PC) is granted to export oriented industry usually garments industry to finance their expenses for Utility, Salaries, Wages etc. the quantum of packing credit is usually 10 % to 155% of the value of the export L/C.

Back-to-Back Credit Facility (BTB)

Back-to-Back Credit Facility (BTB) is issued to import raw materials for export –oriented industry usually of garments. The primary security of Back-to-Back Credit (BTB) is export L/C usually the quantum of Back-to-Back Credit (BTB) L/C is 75% of the value of Master L/C.

Findings:

- In year 2011 import of motijheel branch of AIBL was in highest position where the amount was TK.1139.17 crore.

- In year 2011 the export through motijheel branch of AIBL Bank Ltd was in good position. Motijheel Br of AIBL in 2011 there was a highest position and it was TK.1139.17 crore.

- In 2010 the position was not good of motijheel branch of AIBL. In 2010 there was TK.848.5376 crore.

- Inward remittance has not seriously affected by economic crisis as other foreign exchange activities. Though the growth rate has slightly decreased, still now it is representing a positive growth.

- The export of huge manpower in the different country is the main strength of the inward remittance that comes through AIBL.

- Total import of the branch is less then total export, if we express import as percentage of export than we can see Import is only 25% to 34% of Export.

- Letter of credit (L/C) opening system for the importer is not a easy process. For processing of L/C document, it requires huge amount of time and money as well.

- The existing clients of Foreign Exchange activities of the bank get more benefit than newer.

- Though the maximum of the foreign exchange Foreign Exchange clients are giants in nature, the number of clients is very small in the foreign exchange branch.

- There has a lack of manpower in the foreign exchange division. Some important task of foreign exchange division are hampered, even some case not accomplished in due time only because of the crisis of manpower.

- The major sector of Import and Export the foreign exchange branch deal with is the product of readymade garments industry.

- The bank is circulating in a traditional way. The way of serving customer is not up to the mark.

Recommendations:

- The number of exporter and importer who operate through this bank is not enough to achieve the goal. So AIBL should offer more facilities to attract them to be their client.

- In addition with the present services they should include more services. It is badly needed to provide more services to the customer in order to compete in the market.

- Banking is a service-oriented marketing. Its business profit depends on its service quality. That’s why the authority should always be aware about their service quality.

- Foreign exchange department should be fully computerized that the exchange process would be convenient for both the bankers and the clients.

- The Bank should increase there number of branches and foreign exchange department in other branch. Because they can not compete in the market for their few number foreign exchange department.

- Bank should offer more facilities to the customers such as credit card, visa card, ATM machine etc to survive in the competition.

- On-line banking should be introduced for better customer services and to eliminate risk of sending document via post and risk of loss. It also increases quick fund transfer and better satisfaction from customer.

- Proper Banking software should be used to get best benefit from this department.

- Staff meetings and departmental meetings at the branch level must be increased to develop service quality as well as problem solving

- The bank should give an aggressive advertisement campaign to build up a strong image and reputation the potential customer.

- AIBL should use the latest banking technology to provide better services to the customers. It will also attract the customer’s of international banks.

- AIBL should pursue advertising campaign in order to build a strong image among the people. They should carry out aggressive marketing campaign to attract clients.

- AIBL should offer different types of loans to their own staffs immediately after confirming their job. This loan will influence them for better performance.

Conclusion:

During the period of my internship, I got the chance to observe the overall activities of a branch commencing from foreign exchange. I also got the scope to act together with high officials and was informed about their prospects & perceptions about the Bank’s services. During my interaction with the employees & customers, I understood that there is the existence of customer dissatisfaction in some cases. The Bank is developing its general banking & foreign exchange activities day by day with changing industry situation but the rate of change of such speed needs to be increased. The Bank has the opportunity to develop a leadership position in the industry but new significant strategy ought to be made. I would like to say that this internship at AIBL has developed my practical knowledge of Business Administration & made my BBA education more realistic. The concepts & tools used in this report were from accounting & finance related courses. I desire all the best for the Bank.