The performance measurement process starts by defining precisely the services that the organization promises to provide, including the quality or level of service.Performance measurement is the use of statistical evidence to determine progress toward specific defined organizational objectives. This includes both evidence of actual fact, such as measurement of pavement surface smoothness, and measurement of customer perception such as would be accomplished through a customer satisfaction.

Most of us have heard some version of the standard performance measurement cliches: “what gets measured gets done,” “ if you don’t measure results, you can’t tell success from failure and thus you can’t claim or reward success or avoid unintentionally rewarding failure,” “ if you can’t recognize success, you can’t learn from it; if you can’t recognize failure, you can’t correct it,” “if you can’t measure it, you can neither manage it nor improve it,” but what eludes many of us is the easy path to identifying truly strategic measurements without falling back on things that are easier to measure such as input, project or operational process measurements.

Performance Measurement is addressed in detail in Step Five of the Nine Steps to Successmethodology. In this step, Performance Measures are developed for each of the Strategic Objectives. Leading and lagging measures are identified, expected targets and thresholds are established, and baseline and benchmarking data is developed. The focus on Strategic Objectives, which should articulate exactly what the organization is trying to accomplish, is the key to identifying truly strategic measurements.

Strategic performance measures monitor the implementation and effectiveness of an organization’s strategies, determine the gap between actual and targeted performance and determine organization effectiveness and operational efficiency.

Good Performance Measures:

- Provide a way to see if our strategy is working

- Focus employees’ attention on what matters most to success

- Allow measurement of accomplishments, not just of the work that is performed

- Provide a common language for communication

- Are explicitly defined in terms of owner, unit of measure, collection frequency, data quality, expected value(targets), and thresholds

- Are valid, to ensure measurement of the right things

- Are verifiable, to ensure data collection accuracy

Balanced Scorecard Basics:

The balanced scorecard is a strategic planning and management system that is used extensively in business and industry, government, and nonprofit organizations worldwide to align business activities to the vision and strategy of the organization, improve internal and external communications, and monitor organization performance against strategic goals. It was originated by Drs. Robert Kaplan (Harvard Business School) and David Norton as a performance measurement framework that added strategic non-financial performance measures to traditional financial metrics to give managers and executives a more ‘balanced’ view of organizational performance. While the phrase balanced scorecard was coined in the early 1990s, the roots of the this type of approach are deep, and include the pioneering work of General Electric on performance measurement reporting in the 1950’s and the work of French process engineers (who created the Tableau de Bord – literally, a “dashboard” of performance measures) in the early part of the 20th century.

- The balanced scorecard has evolved from its early use as a simple performance measurement framework to a full strategic planning and management system. The “new” balanced scorecard transforms an organization’s strategic plan from an attractive but passive document into the “marching orders” for the organization on a daily basis. It provides a framework that not only provides performance measurements, but helps planners identify what should be done and measured. It enables executives to truly execute their strategies.

- This new approach to strategic management was first detailed in a series of articles and books by Drs. Kaplan and Norton. Recognizing some of the weaknesses and vagueness of previous management approaches, the balanced scorecard approach provides a clear prescription as to what companies should measure in order to ‘balance’ the financial perspective. The balanced scorecard is a management system (not only a measurement system) that enables organizations to clarify their vision and strategy and translate them into action. It provides feedback around both the internal business processes and external outcomes in order to continuously improve strategic performance and results. When fully deployed, the balanced scorecard transforms strategic planning from an academic exercise into the nerve center of an enterprise.

- Kaplan and Norton describe the innovation of the balanced scorecard as follows:

- “The balanced scorecard retains traditional financial measures. But financial measures tell the story of past events, an adequate story for industrial age companies for which investments in long-term capabilities and customer relationships were not critical for success. These financial measures are inadequate, however, for guiding and evaluating the journey that information age companies must make to create future value through investment in customers, suppliers, employees, processes, technology, and innovation.”

Adapted from Robert S. Kaplan and David P. Norton, “Using the Balanced Scorecard as a Strategic Management System,” Harvard Business Review (January-February 1996): 76.

Adapted from Robert S. Kaplan and David P. Norton, “Using the Balanced Scorecard as a Strategic Management System,” Harvard Business Review (January-February 1996): 76.

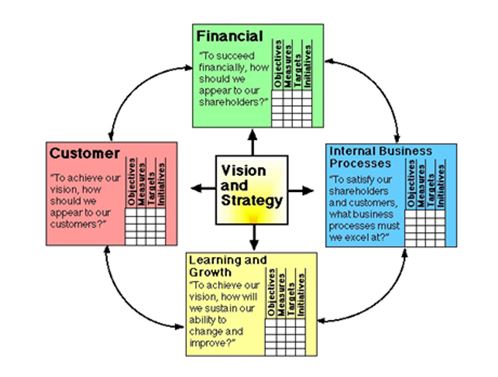

Perspectives :

The balanced scorecard suggests that we view the organization from four perspectives, and to develop metrics, collect data and analyze it relative to each of these perspectives:

The Learning & Growth Perspective:

This perspective includes employee training and corporate cultural attitudes related to both individual and corporate self-improvement. In a knowledge-worker organization, people — the only repository of knowledge — are the main resource. In the current climate of rapid technological change, it is becoming necessary for knowledge workers to be in a continuous learning mode. Metrics can be put into place to guide managers in focusing training funds where they can help the most. In any case, learning and growth constitute the essential foundation for success of any knowledge-worker organization.

Kaplan and Norton emphasize that ‘learning’ is more than ‘training’; it also includes things like mentors and tutors within the organization, as well as that ease of communication among workers that allows them to readily get help on a problem when it is needed. It also includes technological tools; what the Baldrige criteria call “high performance work systems.”

The Business Process Perspective:

This perspective refers to internal business processes. Metrics based on this perspective allow the managers to know how well their business is running, and whether its products and services conform to customer requirements (the mission). These metrics have to be carefully designed by those who know these processes most intimately; with our unique missions these are not something that can be developed by outside consultants.

The Customer Perspective:

Recent management philosophy has shown an increasing realization of the importance of customer focus and customer satisfaction in any business. These are leading indicators: if customers are not satisfied, they will eventually find other suppliers that will meet their needs. Poor performance from this perspective is thus a leading indicator of future decline, even though the current financial picture may look good.

In developing metrics for satisfaction, customers should be analyzed in terms of kinds of customers and the kinds of processes for which we are providing a product or service to those customer groups.

The Financial Perspective:

Kaplan and Norton do not disregard the traditional need for financial data. Timely and accurate funding data will always be a priority, and managers will do whatever necessary to provide it. In fact, often there is more than enough handling and processing of financial data. With the implementation of a corporate database, it is hoped that more of the processing can be centralized and automated. But the point is that the current emphasis on financials leads to the “unbalanced” situation with regard to other perspectives. There is perhaps a need to include additional financial-related data, such as risk assessment and cost-benefit data, in this category.

Strategy Mapping:

Strategy maps are communication tools used to tell a story of how value is created for the organization. They show a logical, step-by-step connection between strategic objectives (shown as ovals on the map) in the form of a cause-and-effect chain. Generally speaking, improving performance in the objectives found in the Learning & Growth perspective (the bottom row) enables the organization to improve its Internal Process perspective Objectives (the next row up), which in turn enables the organization to create desirable results in the Customer and Financial perspectives (the top two rows).

Balanced Scorecard Software:

The balanced scorecard is not a piece of software. Unfortunately, many people believe that implementing software amounts to implementing a balanced scorecard. Once a scorecard has been developed and implemented, however, performance management software can be used to get the right performance information to the right people at the right time. Automation adds structure and discipline to implementing the Balanced Scorecard system, helps transform disparate corporate data into information and knowledge, and helps communicate performance information. The Balanced Scorecard Institute formally recommends the System TMdeveloped by Spider Strategies and co-marketed by the Institute.