BRAC Bank is the first local commercial banks that proving online banking service to its customers from the very beginning of its starts. BRAC Bank, for the first time among local commercial bank, starts providing unsecured loan facilities to salaried person, doctors, teachers, students and businessman as well all over the country. There are two processes of Banking “Branch Banking” and “Alternative Banking” in Brac Bank Ltd. Telesales is the part of alternative banking.

In Bangladesh telesales is firstly used in 1999 but Brac bank firstly launched their telesales department on 16 September 2006 in a small range. But now it develops vastly with 180 employees (from them eighty are female and rest hundred are male). It provides a different kind of service directly to the customers or the persons who are going to be customers. On the other hand, a customer takes the necessary and updates information and solves problems without a physical presence. The BE of telesales department plays a vital role to achieve the goal of the bank.

Introduction:

Banking constitutes an important segment of the financial infrastructure of any company. Generally, banking means deposit mobilization and development of those deposits into advances or investments in different sectors. That’s means bank collect deposit at lowest possible interest and provide loan and opportunity at highest interest. Between the two interests is the profit for bank. There are two type of banking that was commercial banking and another is investment banking. Commercial bank rise fund by collecting deposits from customer and business that use to make loan and customer at high interest for maximize profit. BRAC bank is one of the most popular and profitable commercial bank in Bangladesh.

As a kid banking industry, BRAC Bank Limited was established in June 2001. Performing well as it has acquired as it has assets and human resources of higher quality. BRAC Bank Limited will be more effective in our economy by adopting the modern financial technology by extending their activities in human and social welfare.

Background of the study:

Through this report an individual can expect to have a good knowledge and understanding on the various methods of operation performed by BRAC Bank Limited particularly in the area of Financial Institutional Services. From the last three months of the bank’s disbursement, everything is tried to include in precise form. I have tried my level best to put more emphasis on the Overall activities of telesales department this report is to be used only for the academic purpose. I have collected all the necessary and relevant data from various primary, secondary and tertiary sources. After three months long hard labor, it has become possible for me to make the report comprehensive and factual.

Significance:

This report is the result of three months internship in BRAC BANK LIMITED. I enter as an internee in BRAC BANK LIMITED beginning from 1st March. 2009 to 31st May 2009. And I have completed this internship period successfully. This internship report contains all the knowledge that I gather at the time of my internee in BRAC BANK LIMITED. In this internee time I noticed that they work completed day to day. They work hard and soul. My topic is Penal Calculation for Consumer loan of BRAC Bank. All these information will help the management to the study. Besides, it would be a great opportunity for me to get familiar with this system. So this study is very significant for both the company and me. They satisfy my work and give a opportunity for job.

Objective of the Report:

Broad Objectives:

The broad objective of this report is to study the overall activities and service providing process of Telesales Department of BRAC Bank Ltd.

Specific objectives:

- To know the activities of Telesales department in BRAC Bank Ltd.

- To know the products and services offered by BRAC Bank Ltd.

- To know the concept of Telesales and its impact in overall economy of Bangladesh

- To gain practical experience that will be helpful for my BBA program

- To identify differences between theory and practice by working directly in the bank.

- To know the terms and conditions of Retail or consumers loans and deposit.

- To know the work process and monitoring system of Telesales Department.

Scope of the Report:

Scope of the study is quite clear. Since Telesales Department is dealing with all types of loan & deposit activities in the bank, studying these core themes, Opportunities are there to learn other aspects of RETAIL or Consumer matters.

- Concept of Telesales and its impact in overall economy of Bangladesh

- Importance of Telesales in context of Bangladesh

- Pioneer’s strategy regarding Telesales Department

Methodology of the Report:

The report is basically prepared on the basis of my experiences with BRAC Bank Ltd. The data have been used both as primary and secondary data.

Sources of Data Collection:

The basic sources of data collection based on primary and secondary which used in the preparation of this report is obtained when I went to Telesales Department of BRAC Bank Ltd., Haque Tower (4th floor), Tejgaon.

Primary data sources:

- Conversations with Associate Managers both asset and liabilities.

- Focus group meetings

- Direct observation

- Informal discussion

Secondary data sources:

- Operational manual

- Official Website

- Banking journals

- BBL newsletters

- Account statement

Data Analysis and Reporting:

Both the qualitative (such as SWOT analysis) and quantitative tools are used to analyze the gathered data and different types of computer software’s are used for reporting the gathered information from the analysis, such as – Microsoft word, Microsoft Excel, Microsoft PowerPoint.

Organization Profile- an Overview of BRAC Bank Limited

BRAC Bank Limited, with institutional shareholdings by BRAC, International Finance Corporation (IFC) and Shorecap International, has been the fastest growing Bank in 2004 and 2005. The Bank operates under a “double bottom line” agenda where profit and social responsibility go hand in hand as it strives towards a poverty-free, enlightened Bangladesh.

A fully operational Commercial Bank, BRAC Bank focuses on pursuing unexplored market niches in the Small and Medium Enterprise Business, which hitherto has remained largely untapped within the country. In the last five years of operation, the Bank has disbursed over BDT 2500 core in loans to nearly 1,50,000 small and medium entrepreneurs. The management of the Bank believes that this sector of the economy can contribute the most to the rapid generation of employment in Bangladesh. Since inception in July 2001, the Bank’s footprint has grown to 56 branches, 350 RETAIL unit offices and 122 ATM sites across the country, In the years ahead BRAC Bank expects to introduce many more services and products as well as add a wider network of RETAIL unit offices, Retail Branches, and ATMs and paid up capital of the same bank is Tk 500 million.

Background of the Organization:

BRAC Bank Limited is a scheduled commercial bank in Bangladesh. It established in Bangladesh under the Banking Companies Act, 1991 and incorporated as private limited company on 20 May 1999 under the Companies Act, 1994. The primary objective of the Bank is to provide all kinds of banking business. At the very beginning the Bank faced some legal obligation because the High Court of Bangladesh suspended activity of the Bank and it could fail to start its operations till 03 June 2001. Eventually, the judgment of the High Court was set aside and dismissed by the Appellate Division of the Supreme Court on 04 June 2001 and the Bank has started its operations from July 04, 2001.

There are two process of Banking “Branch Banking” and “Alternative Banking” in Brac Bank Ltd. Telesales is the part of alternative banking and they are the part of RETAIL Division. In Bangladesh telesales is firstly used in 1999 but Brac bank firstly lunched their telesales department in 16 September, 2006 in a small range. But now it develops vastly with 180 employees (from them eighty are female and rest hundred are male)

Corporate Vision:

Building a profitable and socially responsible financial institution focused on Markets and Business with growth potential, thereby assisting BRAC and stakeholders build a “just, enlightened, healthy, democratic and poverty free Bangladesh.

- Corporate Mission:

Achieve efficient synergies between the bank’s Branches, RETAIL Unit Offices and BRAC field offices for delivery of Remittance and Bank’s other products and services.

Goals:

BRAC Bank will be the absolute market leader in the number of loans given to small and medium sized enterprises through out Bangladesh. It will be a world-class organization in terms of service quality and establishing relationships that help its customers to develop and grow successfully. It will be the Bank of choice both for its employees and its customers, the model bank in this part of the world.

Objectives of the Bank:

- Building a strong customer focus and relationship based on integrity, superior service.

- To creating an honest, open and enabling environment

- To value and respect people and make decisions based on merit

- To strive for profit & sound growth

- To value the fact that they are the members of the BRAC family – committed to the creation of employment opportunities across Bangladesh.

- To work as a team to serve the best interest of our owners

- To relentless in pursuit of business innovation and improvement

- To base recognition and reward on performance

- To encourage the new entrepreneurs for investment and thus to develop the country’s industrial sector and contribute to the economic development.

Achievements:

- Fastest growing bank in the country for the last two years

- Leader in SME financing through 350 offices

- Biggest suit of personal banking & SME products

- Large ATM (Automated Teller Machine) & POS (Point of sales) network

Departments of BRAC Bank Limited:

- Human Resources Department

- Financial Administration Department

- Asset Operations Department

- Credit Division

- RETAIL Division (Telesales & Direct sales)

- Internal Control & Compliance Department

History of Telesales:

Some people believe that in the 1950s, Dial America Marketing, Inc became the first company completely dedicated to inbound and outbound telephone sales and services. The company, spun-off and sold by Time, Inc. magazine in 1976, became the largest provider of telephone sales and services to magazine publishing companies. The term telemarketing was first used extensively in the late 1970s to describe Bell System communications which related to new uses for the outbound WATS and inbound Toll-free services.

Telesales Department of Brac Bank Ltd:

There are two processes of Banking “Branch Banking” and “Alternative Banking” in Brac Bank Ltd. Telesales is the part of alternative banking.

In Bangladesh telesales is firstly used in 1999 but Brac bank firstly launched their telesales department on 16 September 2006 in a small range. But now it develops vastly with 180 employees (from them eighty are female and rest hundred are male). It provides a different kind of service directly to the customers or the persons who are going to be customers. On the other hand, a customer takes the necessary and updates information and solves problems without a physical presence. The BE of telesales department plays a vital role to achieve the goal of a bank. The both male and female BE call new and existing customers and encourage them to open an account FDR, DPS, student file in our bank or help them to get a loan if they want. If the customer is being satisfied to hare the offer of BE, then he fixed a date to open an account and one of the BE (must be male) go to the nearest branch of customer and help the customer to fill up the Customer Relationship From and singe as a customer introduce.

Location of Telesales Office:

Telesales Center

- 191/A (4th Floor), Tejgan, Dhaka-1208.

- Tel: +880-2-881 4441

- Fax: +880-2-989 1915

- E-mail: info@bracbank

The slogan of Telesales Department:

“Sell at least Three Products to an Individual Customer

Categories:

There are two major categories of telemarketing. These are

- Business-to-business.

- Business-to-consumer.

The Direct selling Department of Standard Chartered Bank maintains both types of Telemarketing. But the Telesales Department of BRAC Bank Ltd. deals with retail customer and provides them retail banking activities. The reason is that BRAC Bank Ltd has another corporate banking department named Direct Selling Department.

Customer Segmentation of Telesales:

Though telesales department is a part of Retail Banking they target their customer in four categories, these are as follows:

- Businessman (SME)

- Private Customer

- Student

- House Wife

How to Use Cash Deposit Machine:

- Maximum 50 but suggest the customer for 40 notes maximum.

- Complete the information requested at the back of envelopes.

- Please, cheque(s) and cash inside envelop and seal envelop.

- Don’t place any coins in envelop and follow the instruction screen.

- Take transaction input details and keep for the future reference.

- Insert envelop into the slot.

- Take transaction input detail and keep for the future reference.

What is Telesales?

Telemarketing (known as telesales in the UK and Ireland) is a method of direct marketing in which a salesperson solicits to prospective customers to buy products or services, either over the phone or through a subsequent face to face or Web conferencing appointment scheduled during the call.

Telemarketing can also include recorded sales pitches programmed to be played over the phone via automatic dialing. Telemarketing has come under fire in recent years, being viewed as an annoyance by many.

Telesales Activities:

- Provide new information.

- Encourage people to open an account or take a loan.

- Highlight the superiority of the bank to the customer.

- Help customer to open an account.

- Help customer to get a loan.

- Saturday banking information

- Inform customer about the new product of the bank

- Inform customer of all fees and charge.

- Student file query.

- Follow up the customer

- Balance Inquiry

- Account Statement

- Loan information

- Cheque Status

- Lost Card Reporting

- Credit Card Related Service.

- Information on Co-Brand Cards.

- Current interest rate for all products.

- POS point location

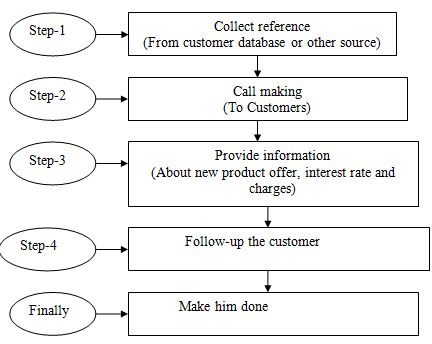

The process of Telesales:

The process of Telesales occurs in some following steps:

Step-1: Collect Reference

The first step of sales via telephone is to collect customer number or address to contract. In this stage, Business Executive collect address or contract number from their relative, friends or other customer’s database (it may be inside or outside database of the bank).

Step-2: Call Making

In this stage Business Executives contract to the customer via mobile or telephone and introduce themselves such like that “Good morning sir, I am …..from Brac Bank”. Then they ask some bank related question like; have you any account in Brac Bank?

Step-3: Provide information

After hearing the answer of the customer the BE can easily understand what information is needed to the customer and they provide them perfectly and correctly. If the customer is the existing customer, Business Executive provides information about new products, offers, and interest rate or the person is going to be a customer he/ she provide him/ her about all products, services, offers, and interest.

Step-4: Follow-up the customer

In this stage, they call again those customers whose they provide information before and follow up them to take the product (means to open an account, FDR, DPS, and loan).

Finally: Make him done

Finally, they encourage a customer to make him done. That means the customers have come to his/ her nearest branch and the BE go to the same brunch and help him/ her to fill up the customer relationship from and open the account, DPS, FDR, and to get a loan.

Advantages of Telesales:

- Less customer time consuming and expense consuming

- The customer gets all the correct information properly.

- Telesales deliveries information on bank service (i.e. evening banking, number of branches, ATM, POS etc.)

- Telesales provides information about the product.

- Encourage exciting customer to take new product

- Increase a total number of sales of Brac Bank.

- No hassle, no fuss.

- Encourage new customer to open an account or to take a loan from the bank.

Disadvantages of Telesales:

Customer face lots of problems because of the phone of a business executive. They are very much angry on phone banking. Sometimes customers do not receive the unknown phone because of their own work. That’s why the system is a hazard. Though telesales is the new concept in Bangladesh most of the customers do not aware of it. So they are ready to come branch but not to talk with BE via phone. Many customers don’t believe us and go to the CSO to open an account or collect information.

Call Manner:

Business Executives of telesales have to maintain a specific call manner or call process to provide better service to the valued clients, which are given below:

- Take permission from customer for holding

- Monogramming of call.

- Avoid excuse.

- Giving the caller subdividing communication.

- Giving spoken feedback of customer in a positive manner.

- Avoiding mouth noise.

- Using question, listening, summarizing

Agent Attitudes:

- Maintain call structure.

- Confidence voice.

- Spoken feedback

- Different between good and great service

- Voice conversation must be clear and clean.

- Strong personality.

- Smiling face.

- Cheerful

- Patience

- Good listing skill.

Performance Evaluation of Telesales Department:

| Performance | ||||

| Evaluation | ||||

| 2008 | 2009 | |||

| Month | No. of Calls | Feedback | No. of Calls | Feedback |

| January | 35720 | 17545 | 151013 | 56124 |

| February | 39294 | 14261 | 146879 | 23541 |

| March | 42275 | 13210 | 115349 | 45121 |

| April | 46157 | 32100 | 113248 | 12456 |

| May | 42320 | 12012 | 110798 | 36541 |

| June | 38128 | 12245 | ||

| July | 51015 | 12413 | ||

| August | 56177 | 18941 | ||

| September | 73706 | 19875 | ||

| October | 84857 | 20012 | ||

| November | 120503 | 23120 | ||

| December | 121317 | 34512 | ||

| Total | 751469 | 230246 | 637287 | 173783 |

Interpretation: about above chart

According to the above chart, we can see that the number of calls in 2009 is higher than the months of 2008. But the feedback of 2009 is lower than the months of 2008. The main reason for this lowest feedback is job switching and became permanent of the senior BEs. Although HR department of BRAC Bank Limited has recruited new BEs, they are not trained enough as like as the senior BEs.

Good Customer Service:

Customer service agents have to occupy some skill and abilities to provide the better services to the customer that are given below:

- Opening with Smiling Face.

- Positive Attitude.

- Helping Mode.

- Good Pronunciation.

- An answer to the Point.

- Customer Need Understand.

- Listening Power.

- Give Alternative Solution.

- Don’t interrupt with the customer.

- Trademark Closing.

- Motivational Power.

- Be free & Go Close to the customers

Bad Customer Service:

- Opening without a smile.

- Lack of listening.

- Don’t Understand the customer

- Lack of Patient.

- Unnecessary Talking.

- Bad Pronunciation.

- Wrong Information.

- Rude voice.

- Interrupt the customer.

- Don’t enjoy the conversation.

The responsibility for the Customer Service Agent Service:

Quality:

- Ensure proper opening and closing of conversation with the customer.

- Maintain courtesy & politeness while conversing with customer

- Ensure one-stop service provided to customers

- Handle customer complaints with diligence.

- Ensure mystery shopper rating is achieved as per standard.

Product knowledge:

- Have a thorough knowledge of BBL products and camping.

- Be updated on the new product launches & latest marketing.

- Perform up to mark on the monthly quiz (Min 80%).

Accuracy:

- Ensure customer queries are responded to efficiently and accurately.

- Ensure action & stop payment of cheques and blocking of ATM are processed accurately and promptly.

- Ensure accuracy is maintained while processing customer instructions. Teamwork.

- Maintain cooperative and friendly attitudes others BE.

- Guide and train new BE.

General:

- Ensure logged in time & break time is maintained as per requirement and punctuality maintained.

- Handle peak hour pressure, downtimes efficiently (other jobs should be done during off-peak hrs).

- Avoid loud conversation/ laughter and food while logged-in.

Customer compliments:

- The valued clients are pleased with getting services through Tele Banking.

- The interacting process of the “Tele Banking” agent is highly appreciated by the customers

- The customers appreciate the new promotional packages for any product.

- What a great process to serve the customer service it is through the Tele Banking as a local in Bangladesh.

- Agents of the Tele Banking department are different.

- TeleBanking agents try to solve the problem instantly.

Customer’s complaints:

The valued clients don’t interest to aspect the new delivery process of “cheque Books” and “ATM Cards”

- Our valued customers don’t to accept the cheque activation process.

- The valued clients want to get a good cooperation from the branch

- The sales executives do not get the complete information especially about the charges of any product

- The branch employees do not inform the valued customer about his / her cheque which is sent for collection. They always consume much time also.

- The customer can’t not login “Internet Banking” frequently.

- Bills payable Machine consumes more time to credit amount of customers an account.

- The Money, which is accepted by ATM booth. is credited amount after a long period of time

- Holding problem: customer hold for a long time.

- After long time call waiting for the call will be automatically disconnected

Customer’s Suggestion:

- Service quality should be developed.

- Service should be easy and faster.

- More Branch and ATM booth.

- Word of Business Executive should be clear and attractive.

- Provide correct and effective information.

- Sound knowledge of the product of BE.

Sales Volume of Telesales Department:

| Sales Volume of Telesales Department | |||||||||

| March | April | May | |||||||

| Product | Number | Amount | Number | Amount | Number | Amount | |||

| Account | 350 | 20010000 | 363 | 20045000 | 250 | 19100000 | |||

| Loan | 45 | 15000000 | 46 | 18500000 | 39 | 13370000 | |||

| FDR | 67 | 19910000 | 71 | 22011000 | 58 | 15823000 | |||

Interpretation:

If we see the figure we can easily understand that the sales volumes of Telesales Department have been fluxed in every month. In the month of April, both the amount & the number of the sales of the products have been increased. But in May both the amount & the number of the sales of the products have been decreased, because of the change in interest rate both loan & deposit product.

Telesales Related Services:

Telesales services are divided into following parts. These are given below:

Account Related Service

- Balance Query

- Transaction Details

- Loan account Details

- ATM Card Related Service

Product Related Service:

- Accounts

- Deposit Product

- Card Product

- Loan Product

Banking Related Service:

- Evening Banking

- Saturday Banking

- Internet Banking

Account Related Service:

When a customer wants to know about their account balance, transaction details, and loan account details and stop or lose their ATM card & checkbook we provide a guideline to the customers. For account Balance and loan account information, Business Executive ask customer following things. Such as:

- Account name

- Date of birth

- Mobile number

- Communication address

If a customer fails to answer the question properly, they can not get the account related service.

Product Related Service:

Different types of Account:

Brac Bank Ltd. is now offering different dynamic products for mobilizing the saving of general people are as follows:

Savings Account:

Any Individual, self-employed, proprietorship, club, charity, and the private company can open this account. Its opening balance is TK: 15000 & ROI 5.5% p.a. (interest credit to account – half yearly). Its relationship fee: TK. 920, Card Fee: TK.598 yearly.

Current Account:

It is a non-interest bearing current account. Any Individual, self-employed, proprietorship, club, charity, and the private company can open this account. Its opening balance is TK: 15000. Its relationship fee: TK. 920, Card Fee: TK.598 yearly.

Ezee Account:

Ezee Account is an interest-bearing non-cheque Account. Individual & corporate people can open this account. Its opening balance is TK: 10000 & ROI 4% p.a. (June 30th and 31st December) Card Fee: TK.598 yearly. The customer can get 12-page cheque-books on request.

Bizness Account:

Small and medium-sized business (only sole proprietorship business) can open this account. It’s an interest bearing current account. Its opening balance is TK: 10000 & ROI 4% p.a. (interest credit to account – half yearly). Bizness Account will be given opened in the name of the business & Card will be given in the name of the proprietor. Its fees & charges: TK. 1000 =15% vat =1150.00 per year.

TBSA Account:

TBSA means Triple Benefit Saving Account. In this account three benefits are offered to the customers. These benefits include unlimited transaction, maximum 8% interest & totally charge free account. To get this benefit customer should keep at least TK. 50000 averagely in every month. The opening balance of this account is TK. 50000. If a customer fails to keep monthly TK. 50000 in their account, he will punish and cutoff TK. 750 for half yearly.

Salary Account:

MNCs, LLCs, NGOs, Large Proprietorship, Partnership Firm & Minimum 10 permanent staff employed at any point in time. Minimum monthly total payroll TK. 100k and an average salary per employ of TK. 10000 per month. Its interest rate is 4% p.a. interest credited twice a year and Card Fee: TK. 345 yearly.

Account Opening Requirements:

For Salaried

- 2 pp size photograph – Account Holder.

- 1 pp size photograph – Nominee.

- An Introducer from of BRAC Bank is needed.

- Any identification documents such as current valid passport, valid driving license or voter ID card.

- Proof of residence – copy of a utility bill (i.e. BTTI, DESCO, GAS).

Additional for Business:

- 6.Trade License

- Copy of Memorandum & articles of the association (For Ltd. company).

- Board of Resolution copy.

- Proof of ID.

- Proof of residence – copy of a utility bill (i.e. BTTI, DESCO, GAS).

Account Opening Requirements:

Bangladeshi Nationals:

- Account Opening Form (AOF) duly completed and signed.

- Passport Copy – 1st 6 pages or a copy of the national ID card.

- Nominee Form.

- Risk assessment profile.

- 2 Copies of photograph duly attested by the introducer.

- 1 Copies of Nominee’s photograph duly attested by the Account Holder.

Non-Resident Bangladeshi:

- Resident Permit / Work permit.

- Copy of the passport

- Passport size photograph – 2 Copies.

- Photograph of the Nominee

- Proof of Address

Deposit Products:

Type of FDR:

General FDR:

| Retail FDR | |||

| Tenor | 100K-<500K | 500K-<5M | 5M and Above |

| 1 months | 7.00% | 7.00% | 7.00% |

| 3 months | 7.50% | 8.50% | 9.00% |

| 6 months | 8.00% | 8.50% | 9.00% |

| 12 months | 9.00% | 9.50% | 9.50% |

| 24 months | 9.00% | 9.00% | 9.00% |

| 36 months | 9.00% | 9.00% | 9.00% |

Freedom Fixed Deposits:

| Freedom Fixed Deposit | |||

| Tenor (months) | 100K-<5M | 5M-< Above | |

| 6 | 8.50% | 9.00% | |

| 12 | 9.00% | 9.25% | |

| 24/36 | 9.00% | 9.25% | |

Interest First FDR:

| Interest First FDR | ||

| 3 months | 100K & Above | 8.50% |

| 6 months | 100K & Above | 8.50% |

| 12 months | 100K & Above | 8.50% |

ABIRAM:

| Principle Amount & Rare of Interest | ||||

| Tenor | 100K-999K | 1000K-4999K | 5000K-9999K | 10000K & + |

| 12 months | 8.50% | 9.00% | 9.00% | 9.00% |

| 24 months | 8.50% | 9.00% | 9.00% | 9.00% |

| 36 months | 8.50% | 9.00% | 9.00% | 9.00% |

DPS:

Deposit Premium scheme’s monthly installment cannot be as low as Tk.500 or any multiplies like Tk.1000, Tk.2500, Tk.5000 and so on. Customers are free to choose the maturity of his or her DPS and they also selected the period of 4 years, 7 years, 11 years and 14 years it’s depending on customer’s convenience.

| Term | Rate of Interest |

| 4 years | 8.50% |

| 7 years | 9.00% |

| 11 years | 9.50% |

| 14 years | 9.75% |

Card Product:

DEBIT VISA CARD:

Visa debit card is a popular mode of withdrawal/payment option. Globally, more visa payment transactions are made using visa debit cards than visa credit cards. With a debit card, the money for each transaction comes directly out of your linked bank account.

Card Number: 4 3 2 1 4 9

Advantages:

- From ATM BDT 50,000 per day but a customer can use 5 times in a day.

- From Brac Bank’s Branch POS BDT 1, 00,000 per day withdrawal limit.

- There would be no fees if the transaction takes taka place in Brac Bank ATMs & POS. But there will be small charges (which is currently $ 1 per transaction) if any cash withdrawal takes place in other Bank’s VISA enable ATMs.

- There will also be no fee if you use the card in other Bank’s merchant POSs.

Annual Fees: BDT 520 + 15% vat = BDT 598.00

Aarong Card:

BRAC Bank Aarong co-branded ATM card is a new variant (product/brand extension) of our existing ATM card, which is designed to leverage the high brand value of Aarong – the most popular retail chain of gift/design house of Bangladesh. This card has similar functionality as our classic BRAC Bank ATM card with the extra advantage of having “Cash BRAC” facility. The holder of the card will get a 5% discount on every purchase at any Aarong outlet. This discount will be directly credited to the cardholder’s account for each purchase at Aarong.

Annual Fee for the Card: The fee is Taka. 575.00 (With 15% VAT)

Alico Card:

BRAC Bank ALICO co-branded ATM card is a new variant (product/brand extension) of our existing ATM card, which is designed to leverage the high brand value of American Life Insurance Company. This card has similar functionality as our classic BRAC Bank ATM card with the extra advantage of having “Insurance Coverage”. The Bank on behalf of the customers will pay the insurance premium.

Annual Fee for the Card: The fee is Taka. 575.00 (With 15% VAT)

Dia Gold Card:

BRAC Bank Dia Gold co-branded ATM card is a new variant (product/brand extension) of our existing ATM card, which is designed to leverage the brand value of Dia Gold. This card has similar functionality as our classic BRAC Bank ATM card with the extra advantage of getting “Discount” for purchasing jewelry items from Dia Gold outlets.

Annual Fee for the Card: The fee is Taka. 575.00 (With 15% VAT)

Loan Products:

Salary Loan:

Keep an extra 15 month’s salary in your pocket. You can get BRAC Bank Salary loan, Loan against your salary. If you are a salaried individual working in Bangladesh, Please read on. Because Salary Loan from BRAC Bank has been designed with just you in our minds.

Who can apply?

- Employed as a regular salaried staff

- Have minimum age of 25 years, max -53 years (at the time of application)

- If you earn a gross monthly salary of Tk. 10000

Doctor’s Loan:

BRAC Bank introducing Doctor’s Loan, an exclusive loan facility for the Doctor’s fraternity. Now practicing Doctor’s can avail this loan very easy to meet their professional needs. So prescribe yourself a dream today. Anti-Headache solution for Doctor’s

Who can apply?

- Having M.B.B.S. with 2 years of experience

- A salaried or a self-employed Doctor’s

- Aged between 25 to 55 years

NoW Loan:

‘You choose while we pay’!! Life is good to make it better when you can enjoy BRAC Bank NoW Loan. In case you need to purchase home appliances, furniture’s, computer or other consumer durables for personal use, we offer you the most appropriate solution with our NoW loan.

Who can apply?

- BRAC Bank account holder aged from 25 to 55

- A salaried employee with minimum monthly income of TK 15, 000

- Employed in your current organization for two years

Car Loan:

Why toy with your dreams when you can own one’, BRAC Bank Car Loan can stop your dreaming and Start driving Whether you want to purchase a brand new car or a reconditioned one, we have the most customer-friendly car loan scheme available for you.

Who can apply?

- Both salaried executives and business persons

- Age between 21 at the time of application to 60 at the time of maturity

- Minimum monthly income BDT 25,000

- Length of service/Age of business: Minimum 2 years

Study Loan:

Your gateway to the world’ BRAC Bank Study Loan gives your child deserves the best education and you have planned it ahead. But worried about financing? BRAC bank has the perfect solution for your child’s future.

Who can apply?

- Parent/ financial guarantor of the student pursuing higher education locally and abroad

- Earning TK 25,000 per month

- Aged between 30 to 60 years

Teachers’ Loan:

Honest profession, Honest Service’. BRAC Bank Teachers’ Loan provides a wedding or a dream holiday, financing a business or surviving an emergency, Teachers Loan can be yours just within three days of application!

Who can apply?

- A teacher of any reputed school or university

- Have a minimum length of service record of at least two years

- Have a minimum net salary of Tk.. 5000

- Have a minimum age of 23 years

Documents for Loan Product:

For Service Person:

- Latest Salary Slip

- Letter of Introduction

- Attested statement of account, bill etc. showing designation & Company’s name

- Bank Statement – last 3 months

- Visiting Card

- Personal Guarantor Required

- Proof of residence

- Proof of ID

For Business Man:

- Last 6 months bank statement

- TIN certificate

- Trade License

- Spouse Guarantee

- Proof of residence

- Business Card

- Personal Guarantor Required

Doctor’s Loan:

- Copy of Registration Certificate

- Employment Certificate

- Pay order of BDT 150 for BMDC certificate verification

Banking Related Service:

Evening Banking Service:

The customer can cash deposit and cash withdrawal in evening banking service. But the customer can withdrawal maximum 1 lacks in evening banking. Its time duration is 3 p.m.-8p.m. No. customer service is given in this time duration. Some branches have given these services such as:

- Gulshan Branch

- Banani Branch

- Nawabpur Branch

- Satmoszid Branch

- Rampura Branch

- Zindabazar Branch

- Agrabad Branch

- Mirpur Branch

- Uttara,

- Momin Road Branch

- Mirpur Branch

- Moghbazar Branch

Saturday Banking Services:

Cash withdrawal, deposit, pay orders & only welcome A/C is opened in Saturday banking. Some branches give this services such as:

- Gulshan Branch

- Agrabad Branch

- Motijheel Branch

SWOT Analysis

SWOT means Strength, Weakness, Opportunity, and Threats. Basically, Strength and weaknesses are forms influenced and calculated by organizational internal factors. Opportunity and Threats are influenced and calculated by external environmental factors.

S-Strengths:

- The wide range of service line.

- Excellent working environment.

- The banking service is easily accessible & feasible.

- Higher profitability.

- The bank launched several deposit schemes, which have been appreciated by the customers resulting growth of deposit of bank.

- The bank has earned customers loyalty as well as organization loyalty. The bank has also committed to maintaining quality services to the client.

W-Weaknesses:

- Lack of proper motivation, training and job rotation for new employees.

- Insufficient space & equivalent of office.

- Lack of promotional objective & strategies.

- Lack of experienced employee in junior level management.

O-Opportunities:

- To increasing, skilled customer bank can be earned more profit

- The bank will go for immediate automation of all branches through the computer network.

- Deposit stiff competition among bank operating in Bangladesh, both foreign & local.

T-Threats:

- Increase competition in the market for quality service for other banks.

- The opening of the branches & ATM Booth of new private banks & foreign banks the competition will be intensified.

- More policies of Bangladesh bank & lowering the bank rate by Bangladesh Bank, BRAC Bank Ltd. reduce the lending rate.

Learning Point:

It’s very difficult for anyone to mention all of his learning about three months internship period in his internship report. But I tried my best to mention the following thing which I have learned during these three months:

- The overall retail products and services of the bank and the criteria which have to fulfill to achieve it.

- What are DBR (Debt Burden Ratio) and the calculating process of DBR?

- Activities & responsibilities of the employees of Telesales department in BRAC Bank Ltd.

- What is EMI (Earning Monthly Installment) and AMI (Area of Median Income) and how we have to calculate it?

- Meaning and the calculation of the equation of (DBR) = (EMI / AMI) (100)

- How and which ATM Booths customers can use to withdraw and deposit their money easily.

- What is POS and how much money can be withdrawn by the customer within a very short period of time.

- Enterprise selection criteria to provide Retail or consumer’s loan and the necessary papers to make their loan file.

- The work process and monitoring system of Telesales Department in BRAC Bank Ltd.

- Which step we follow to make customers done.

- The rate of interest and an annual charge of various products and ATM cards.

- Evening Banking System, Bank’s products, Saturday Banking, Internet Banking, SMS banking and about the ATM Booth where we can deposit money easily.

Findings & Analysis:

On the basis of previous analysis and practical experience of 3 months internship program, the following findings are observed during the research period:

- Lac of BOPs (Box of Phones) and headphones are provided by the BBL to the Business Executives.

- The absence of proper guideline/ planning of respective job.

- Lack of motivation and training program for entry-level employees and inadequate information provided to the customers.

- Calculation of DBR (Debt Burden Ratio) by using inadequate data and prepare loan file using this calculation.

- Sales volume of telesales department was reduced during the month of May than the month of April in 2009 because increasing the interest rate on the loan and decreasing the interest rate of deposit.

- Highly reduce the rate of interest on deposit and FDR and increase of the yearly charge of account and card create a negative effect on the customers.

- On the other hand, stable rate of interest on loan products become the cause of reducing customers.

- The POS machine of BRAC Bank is not easy to use than Standard Chartered’s POS and some time its will hazard to the customers.

- Inadequate workforce also hampers to the customer to provide better service like HSBC.

- Increasing huge numbers of ATM Booth and POS Help customers to maintain transaction easily.

- Online Banking and phone banking systems of BRAC Bank can help the customer reduce their time to get information without physical representation of them.

- The average number of calls in 2008 is less but the average feedbacks are high. On the other hand, the average number of calls in 2009 is high but the average feedbacks are less.

Conclusion:

A satisfied customer’s statement is more than a thousand commercial advertisements that BRAC Bank Ltd. tries to achieve by providing effective and efficient services. It is a great pleasure to have a practical experience it couldn’t be possible for me to compare the theory with practices. There is a number of commercial banks operating their activities in Bangladesh. BRAC Bank Ltd. is a promising one of them. For the future planning and successful operation in achieving its prime goal in this current competitive environment, BRAC Bank Ltd. always provide potential and dynamic service trough business sector and operating sector. Telesales Department is one of the important department that sells the various products and services of BRAC Bank Ltd.

From the evolution and analysis of the facts and information collected during the period of my internee, it is clear the BRAC Bank Ltd. is promising satisfactory over the last years and growing rapidly preserving a unique position in the banking sector of the country. The bank is gaining improvement in almost all sectors over last years. The bank has all the possibility of becoming one of the leading banks of the country if it maintains this trained of improvement, and I think it will be able to do so.

Recommendation:

As per we know the BRAC Bank Ltd. is a faster-growing bank in Bangladesh and it provides batter and standard service than most of the bank in our country. However, some steps should be taken to increase the performance and productivity of the bank in future which are given below:

- The employees should train enough to provide faster and better service to the customers.

- CSO of brunch should be more attentive to their customers when they are providing their services.

- BBL should increase huge numbers of ATM Booth and Brunch to provide better and faster service to the customers.

- There is totally huge pressure on account opening department, a helping hand should be given for relieving his pressure accurate and proper working.

- To increase their customers they can more be camping with their new products, named TBSA. Because the customer can take this product without any charge and get maximum 8% interest.

- BBL can offer millennium and bilinear scheme like other banks to attract new customers.

- Telesales department should build proper coordination with IT department.

- Motivate the best performer by providing him/ her increment or reward.

- The training program should be taken more seriously and often. Business Executive should be sent for training for the betterment of service.

- Business Executive should Calculate DBR (Debt Burden Ratio) by using adequate data and prepare loan file using this calculation.

- They should care enough about the interest rate for both Loan & deposit’s products and the charges of the account and card. Because they provide loan with 19.5% interest rate, & they cutoff high charges for the account which is higher than SCB.

- To increase their feedback and sell more products via phone they should train up and provide Business Executive modern technology and handsome remuneration.

![Internship Report on Customer Service of IFIC Bank [ Part-4 ]](https://assignmentpoint.com/wp-content/uploads/2013/04/ific-bank-limited-200x100.jpg)